SoFi Bank shattered expectations in November 2025 by becoming the first nationally chartered, FDIC-insured U. S. bank to integrate cryptocurrency trading directly into its app. This move lets users handle SoFi bank crypto trading alongside checking accounts, loans, and investments without switching platforms. For beginners eyeing SoFi bank bitcoin trading or holding assets securely, it's a pragmatic entry point amid surging digital asset interest, where ownership has doubled this year.

Traditional banks have tiptoed around crypto due to regulatory hurdles, but SoFi's national charter and FDIC backing change the game. You get the safety of insured banking with exposure to volatile markets. No more juggling separate apps from unregulated exchanges; everything sits under one roof with institutional-grade security. That said, limitations like no outbound transfers mean you're locked into their ecosystem for now, which suits conservative holders but frustrates power users wanting wallet flexibility.

SoFi Crypto Fees 2025: Transparent but Not the Cheapest

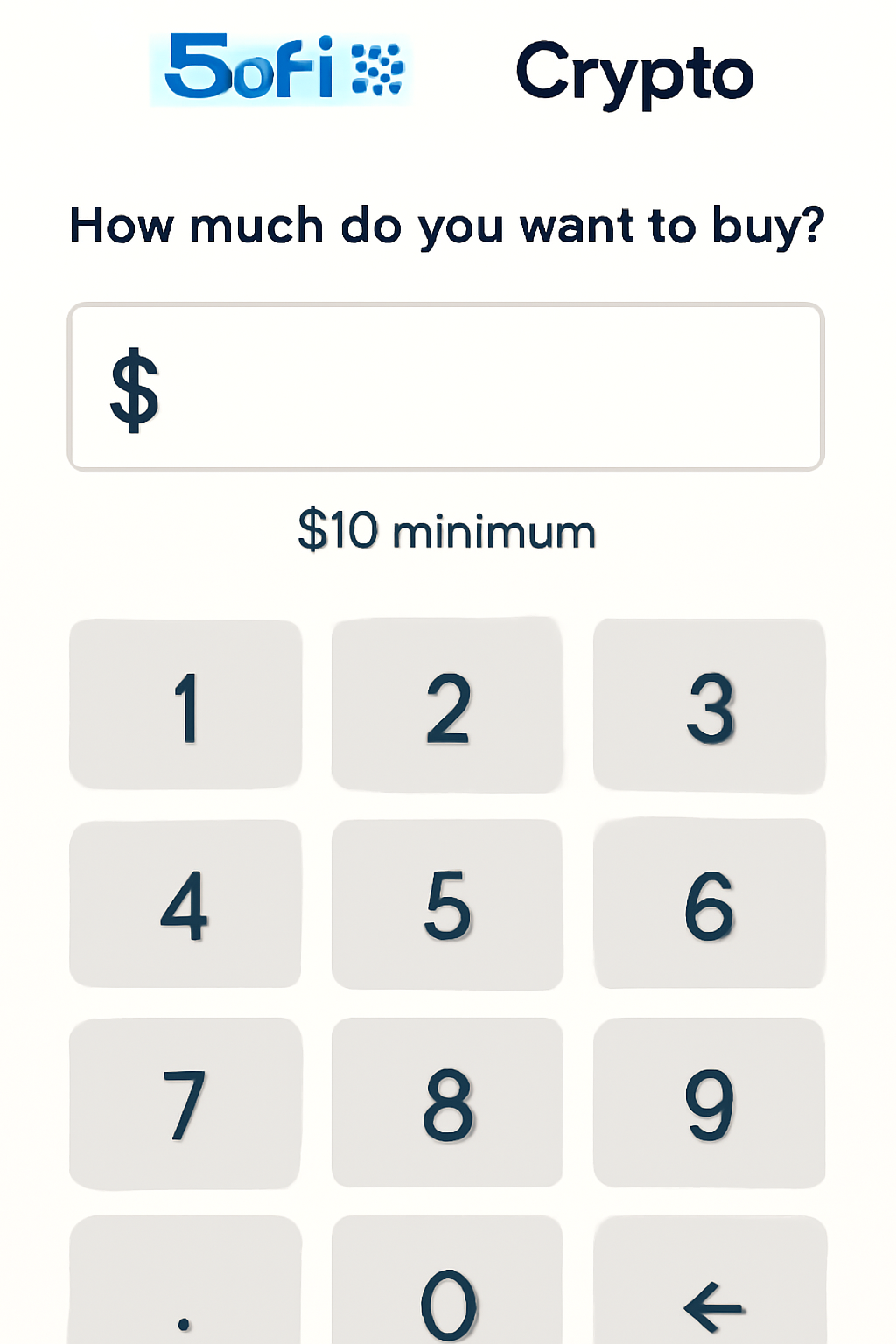

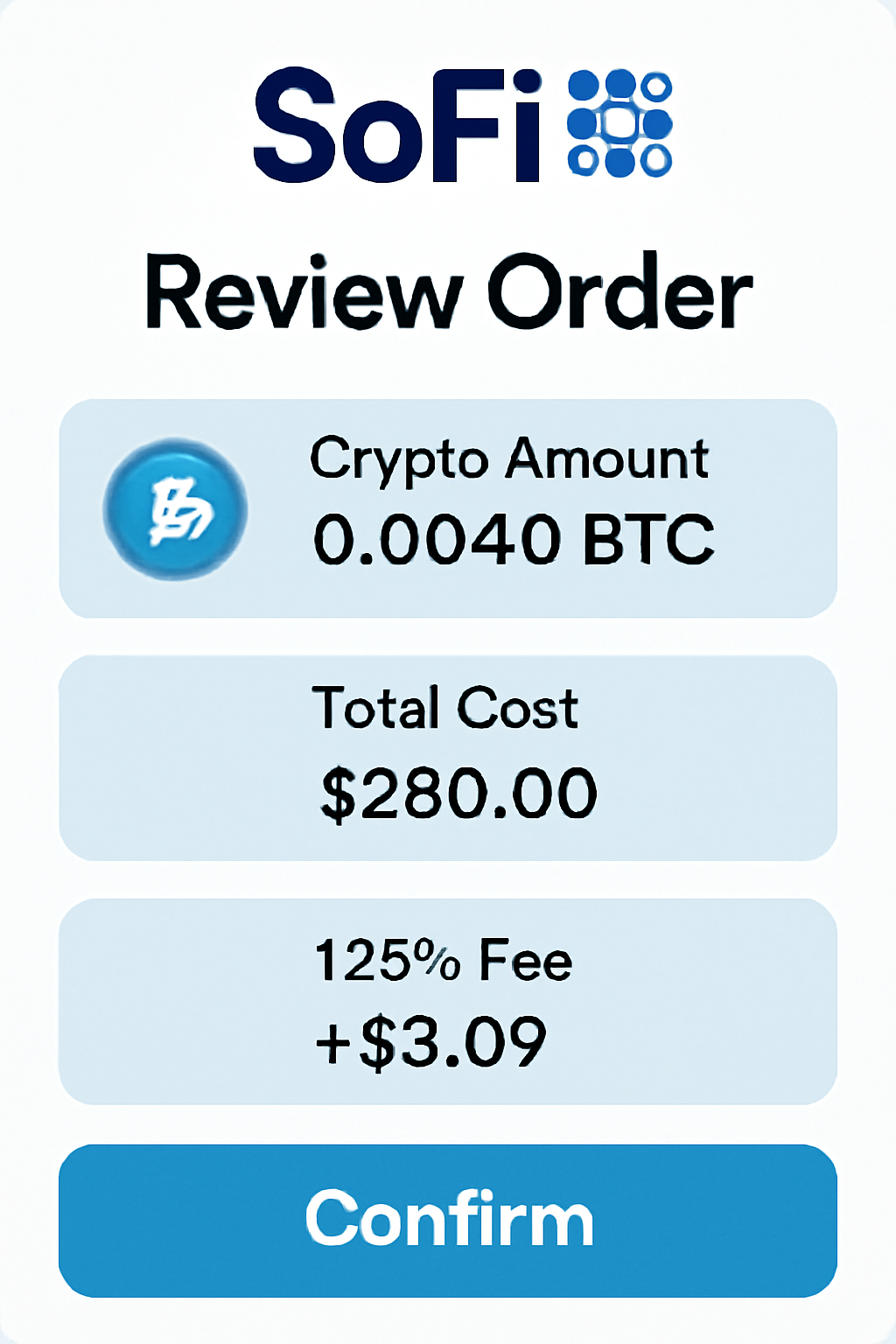

The headline fee for SoFi crypto fees 2025 is a straightforward 1.25% markup baked into every buy or sell. No hidden spreads or tiered structures to decipher; it's added directly to the market price at execution. For a $100 Bitcoin purchase, expect to pay about $101.25 total. Daily limits cap purchases at $50,000, with a $10 minimum order size and zero account minimums to start. This keeps barriers low for testing waters.

Compared to pure-play exchanges, that 1.25% stings on high-volume trades, but SoFi prioritizes simplicity over rock-bottom costs. Active traders might look elsewhere, yet for occasional buys tied to banking, the all-in-one convenience offsets it. No inactivity fees or withdrawal charges apply since you can't move coins out anyway.

SoFi Crypto Fees and Limits

| Fee/Limit | Details |

|---|---|

| Transaction Markup | 1.25% on every cryptocurrency transaction (added to market price) |

| Minimum Order Size | $10 |

| Daily Purchase Limit | $50,000 |

| Account Minimums | None |

| Outbound Transfers | Not supported |

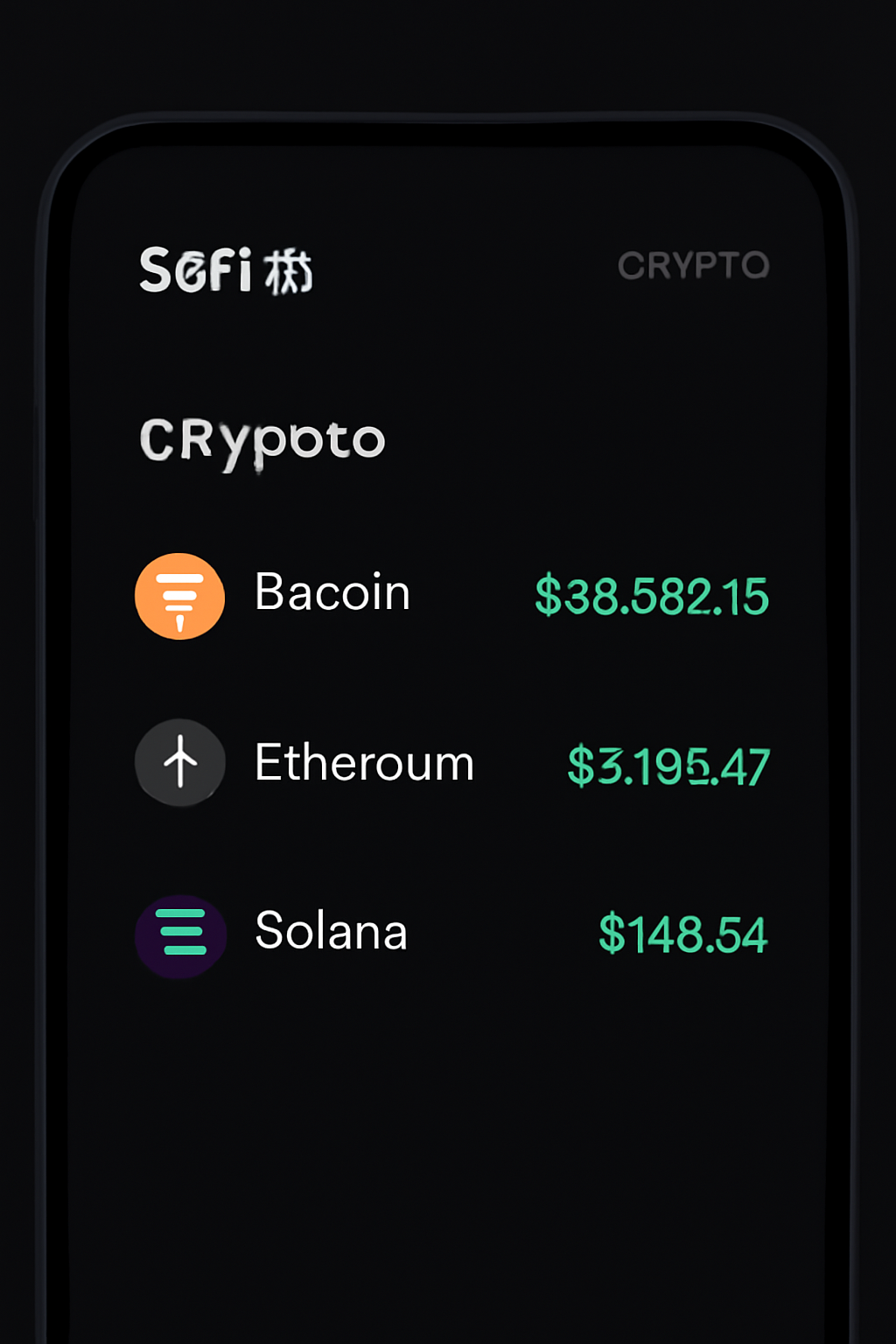

Supported Coins: Starting Strong with Majors

At launch, first US chartered bank crypto services cover Bitcoin (BTC), Ethereum (ETH), and Solana (SOL). These heavy-hitters represent diverse use cases: BTC as digital gold, ETH for smart contracts, and SOL for high-speed DeFi. SoFi plans phased expansions to dozens more, tapping into the gold rush where ownership surges align with their 12.6 million users gaining access by year-end.

Why these three? They dominate market cap and liquidity, minimizing beginner risks from illiquid altcoins. Holding is seamless within the app, with real-time tracking next to your bank balance. Security shines here: as an FDIC member, SoFi employs rigorous compliance, cold storage for assets, and multi-factor authentication standard.

SoFi Hold Crypto Guide: Getting Started as a Beginner

For those new to SoFi hold crypto guide, the platform's in-app education demystifies volatility and strategies without overwhelming jargon. Tutorials cover basics like dollar-cost averaging into BTC during dips, plus pros like faster settlements versus wires. Cons? That no-transfer policy forces commitment, ideal for set-it-and-forget-it types avoiding self-custody pitfalls.

Integration extends further: track crypto performance against your portfolio, use gains for loans, or even future stablecoin remittances. SoFi's betting big, including crypto-linked lending down the line. Risk managers like me appreciate the guardrails; mismanagement lurks in unregulated spots, but here, oversight tempers the wild west.

How to Buy Crypto on SoFi: BTC, ETH, SOL in Minutes

Once you've confirmed that first trade, your holdings appear instantly in the Invest tab, updating live alongside stocks and ETFs. Dollar-cost averaging works smoothly here; set recurring buys to blunt volatility without daily monitoring. For risk-averse beginners, this beats fumbling with seed phrases on decentralized apps.

Security Breakdown: FDIC Perks with Crypto Caveats

SoFi's status as the first US chartered bank crypto platform brings unmatched legitimacy. Fiat balances enjoy FDIC insurance up to $250,000, but crypto holdings do not; they're protected via institutional custody, cold storage, and SOC 2 compliance instead. Multi-factor authentication, biometric logins, and real-time fraud monitoring add layers that unregulated exchanges often skimp on. In my risk frameworks for institutions, this hybrid model scores high: regulated oversight tempers crypto's chaos without diluting upside.

That no-outbound-transfer rule? It's a double-edged sword. It prevents hacks draining your wallet but traps liquidity inside. Fine for long-term holds, problematic if you need DeFi yields or hardware storage. SoFi counters with in-app staking previews for ETH and SOL, hinting at yield features ahead.

SoFi Crypto Security Features

| Security Feature | Status |

|---|---|

| FDIC Insurance on Fiat | ✅ Yes (FDIC-insured bank) |

| Cold Storage for Crypto | ✅ Institutional-level security |

| SOC 2 Audited | ✅ Regulatory compliance standards |

| 2FA and Biometrics | ✅ App-based authentication |

| No External Transfers | ✅ Yes (In-app holding only) |

| In-app Staking | 📈 Coming Soon |

Pros and Cons: Weighing the Trade-offs

Diving deeper into SoFi bank crypto trading, the pros shine for integrated banking users. Seamless fiat ramps mean no ACH delays; buy BTC with your paycheck balance in seconds. Educational pop-ups explain gas fees or halvings contextually, building confidence without leaving the app. At scale, 12.6 million members accessing by year-end could boost liquidity, narrowing spreads over time.

Cons hit harder for pros. The 1.25% markup exceeds Coinbase's 0.5% maker-taker or Robinhood's spreads under 1%, eroding returns on frequent trades. Limited coins frustrate diversification seekers, and no advanced orders like limit buys leave you market-order exposed in swings. Still, for SoFi bank bitcoin trading as a banking adjunct, these pale against the simplicity gain.

Risks from a Risk Manager's View: Pragmatic Guardrails Matter

As an FRM holder who's built frameworks for commodity desks, I see SoFi's setup as a bulwark against common pitfalls. Volatility remains king; BTC can drop 20% overnight, but position sizing via small minimums and daily caps enforces discipline. Regulatory tailwinds help too: post-2025 clarity favors chartered players like SoFi over offshore rivals facing crackdowns.

Key risks? Counterparty dependence on SoFi's custody, plus opportunity costs from locked assets. Mitigate by allocating no more than 5-10% of your portfolio here, rebalancing quarterly against fiat yields. Their roadmap teases crypto-collateralized loans and a USD stablecoin, potentially unlocking borrowing power without selling. That evolution could make SoFi indispensable for hybrid finance.

Compared to peers, SoFi lags in coin count but leads in trust. Kraken offers 200 and assets with transfers; Gemini emphasizes insurance. Yet none match the banking fusion, ideal if you're consolidating life admin. For beginners, start here: low entry, high safety nets. Scale to specialists as skills grow.

SoFi's launch marks a pivot where digital assets join mainstream rails, not side hustles. With expansions inbound, it positions users ahead of the curve in a market doubling yearly. If your risk tolerance aligns with managed exposure, dive in; the guardrails await.

No comments yet. Be the first to share your thoughts!