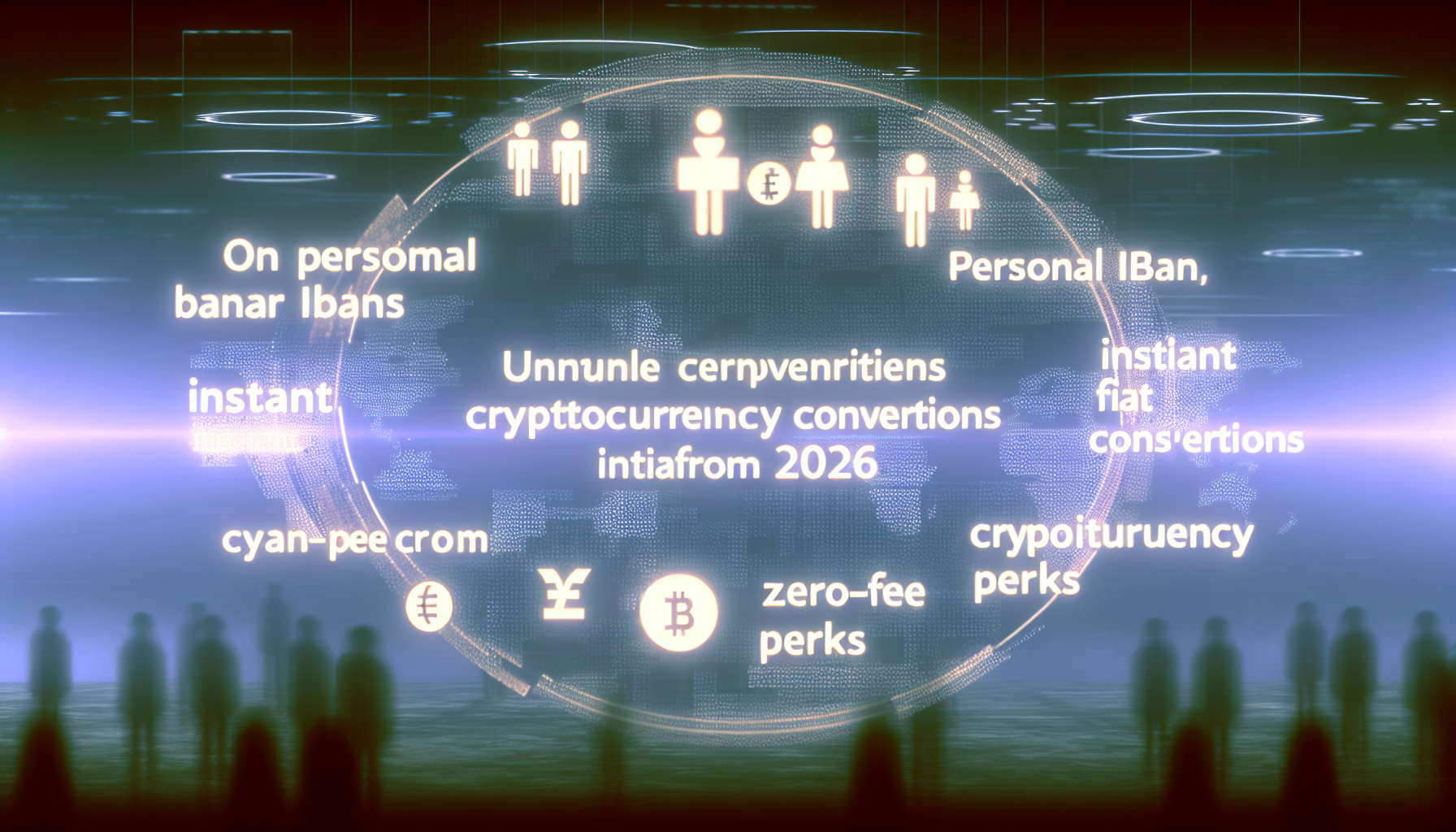

In the ever-evolving landscape of digital finance, Bybit is making a bold leap into the neobank arena with its upcoming MyBank service. Set for a February 2026 launch, this initiative promises Bybit IBAN accounts that support 18 fiat currencies, complete with personal International Bank Account Numbers for seamless cross-border transfers. As a Dubai-based exchange partnering with licensed institutions like Georgia’s Pave Bank, Bybit aims to eliminate the friction between traditional banking and crypto trading. But does this move truly bridge the gap, or is it just another layer of complexity in an already crowded field?

Bybit’s strategy here feels calculated. After weathering the largest hack of 2025, the exchange, led by CEO Ben Zhou, is pivoting toward comprehensive financial services. MyBank users will hold fiat like USD and GBP initially, with plans to expand to 18 currencies total. These accounts enable direct inbound and outbound transfers via IBANs, bypassing the usual delays and fees associated with third-party processors. For crypto enthusiasts tired of juggling multiple apps, this single-interface approach could be a game-changer, fostering faster Bybit fiat to crypto conversion and encouraging broader adoption.

Decoding the Core Features of Bybit MyBank

At its heart, Bybit MyBank targets the pain points of crypto users who still rely heavily on fiat gateways. Imagine depositing euros from a European bank account straight into your Bybit wallet, then instantly swapping for Bitcoin without leaving the platform. The service starts fiat-focused, requiring full KYC verification through both Bybit and its banking partners. This dual-check adds security but might deter privacy-focused traders. Still, the promise of instant crypto conversions positions MyBank as a contender among best crypto banks 2026 hopefuls.

Key MyBank Features

-

Personal IBANs: Users get dedicated International Bank Account Numbers for direct banking integration.

-

18 Fiat Currencies: Support for holding USD, GBP, and 16 others via multi-currency accounts.

-

Instant Fiat-Crypto Swaps: Seamless conversions between fiat deposits and cryptocurrencies.

-

Cross-Border Transfers: Efficient international payments powered by partner banks.

-

KYC-Secured Access: Verified holdings through Bybit and partners like Pave Bank in Georgia.

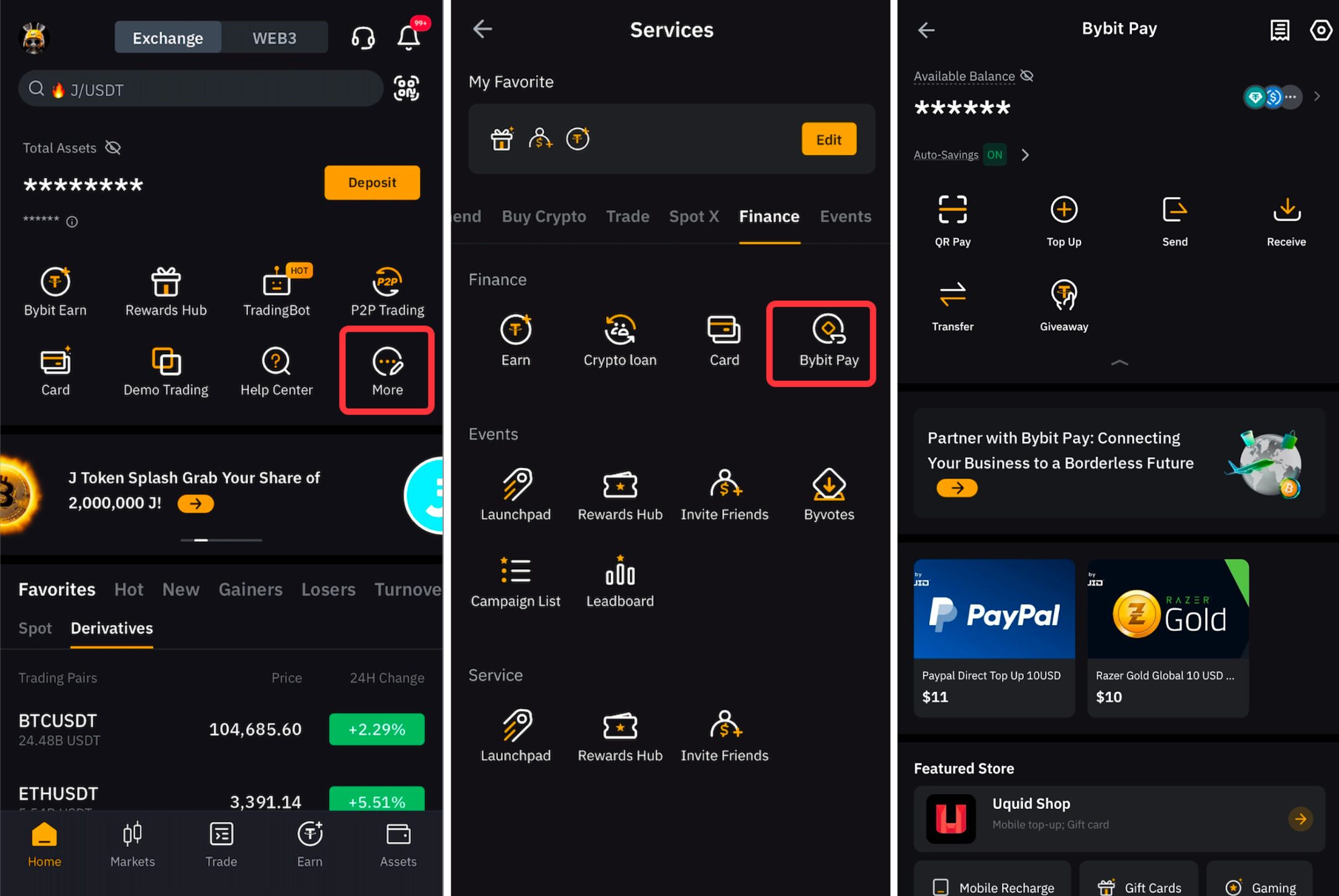

What sets this apart from pure neobanks like Revolut or Wise? Integration with Bybit’s robust trading ecosystem. Users could fund trades directly from MyBank balances, potentially slashing conversion times from days to seconds. Sources like CoinDesk and Bloomberg highlight how this ‘bank-like’ evolution could draw in mainstream users wary of crypto’s volatility. Yet, Reddit discussions in r/CryptoExchange raise valid questions: with fewer intermediaries comes greater responsibility on Bybit’s end for fund safety.

Strategic Partnerships Powering the Launch

Bybit isn’t building MyBank in isolation. Collaborations with regulated banks like Pave Bank ensure compliance and credibility. Pave, based in Georgia, specializes in digital banking rails that support IBAN issuance across multiple jurisdictions. This partnership allows Bybit to offer Bybit banking services without obtaining full banking licenses itself, a clever regulatory workaround. Yahoo Finance reports emphasize the focus on encouraging digital asset adoption through frictionless fiat on-ramps.

PYMNTS and Altcoin Buzz note the rollout’s phased approach: fiat holdings and transfers first, with crypto deposits and withdrawals to follow. This cautious rollout mitigates risks post-2025’s security breach, where Bybit faced significant losses. Investors should watch how these alliances scale; AInvest analyses suggest it’s a scalable path to mainstream integration, but execution will be key amid rising competition from players like Binance and OKX exploring similar hybrid models.

Navigating Security and Accessibility Challenges

Security looms large in any crypto neobank features discussion, especially for Bybit. The 2025 hack, detailed by MEXC, exposed vulnerabilities that CEO Zhou now addresses head-on with MyBank’s bank-partnered infrastructure. Funds in MyBank will likely be held in segregated accounts at licensed institutions, offering FDIC-like protections in supported regions, though details remain pending. Accessibility hinges on KYC completion, which could limit appeal in restrictive jurisdictions but aligns with global anti-money laundering standards.

For businesses, MyBank’s multi-currency IBANs promise efficient payroll and vendor payments in fiat, convertible to crypto at market rates. This blurs lines between Bybit MyBank and traditional corporate banking, potentially capturing a slice of the $10 trillion cross-border payments market. However, early adopters must weigh the novelty against proven alternatives; is Bybit’s track record in trading enough to trust it with everyday banking?

Early feedback from crypto communities underscores these tensions. While enthusiasts praise the convenience, skeptics point to Bybit’s past vulnerabilities as a red flag for holding fiat. Balancing innovation with trust will define MyBank’s trajectory.

Pros and Cons: Weighing Bybit MyBank Against the Competition

To assess MyBank’s place among best crypto banks 2026, consider its edge in unified workflows. Unlike standalone neobanks, it embeds banking directly into a high-volume trading platform, where daily volumes exceed billions. This synergy could slash costs for frequent traders, who often lose 1-2% on external conversions. Yet, competitors like Kraken Bank or Crypto. com’s offerings already provide similar fiat ramps with established licenses.

Bybit MyBank vs Competitors: Key Features Comparison

| Provider | Currencies Supported | IBAN Availability | Crypto Integration | Fees | Security Features |

|---|---|---|---|---|---|

| Bybit MyBank | 18 fiat currencies (e.g., USD, GBP) | Yes ✅ (personal IBANs) | Yes ✅ (instant fiat-to-crypto conversions) | Competitive (details TBD) | KYC required, partnered with licensed banks (e.g., Pave Bank) |

| Revolut | 30+ fiat currencies | Yes ✅ (EUR IBAN, local details) | Yes ✅ (buy/sell/hold crypto) | Variable (crypto spread ~1.5%, free basic transfers) | FCA regulated, 2FA, biometric login, deposit protection |

| Wise | 50+ currencies | Yes ✅ (multi-currency account details/IBAN) | No ❌ | Low transparent fees (0.4-1%) | FCA regulated, 2FA, segregated accounts |

| Crypto.com | 20+ fiat currencies (USD, EUR, GBP+ ) | No ❌ | Yes ✅ (full crypto trading/staking) | Low (trading 0.4%, free fiat deposits) | Cold storage, $750M insurance fund, 2FA |

Revolut excels in everyday spending with crypto cards, but lacks Bybit’s trading depth. Wise dominates cheap transfers yet shuns crypto entirely. Bybit’s pitch: do it all in one app. Drawbacks include unproven fiat custody and potential higher fees during volatile periods. For high-net-worth users, the multi-currency IBANs shine for diversified holdings, but retail users might prefer simpler apps until MyBank proves reliable.

Opinion: MyBank isn’t reinventing banking; it’s supercharging crypto access. If Bybit nails execution, it could lure the next wave of adopters who view fiat as a mere bridge to digital assets. But falter on security, and it risks amplifying 2025’s scars.

How MyBank Reshapes Fiat-to-Crypto On-Ramps

Central to Bybit fiat to crypto conversion is the instant swap mechanism. Picture receiving GBP payroll via IBAN, then converting to USDT in seconds for arbitrage plays. This efficiency targets traders in emerging markets, where banking rails are sluggish. Pave Bank’s involvement ensures SEPA and SWIFT compatibility, broadening reach across Europe and beyond.

Businesses stand to gain most. With 18 currencies at launch, firms can settle international invoices in local fiat, hedge via crypto, all under one KYC umbrella. This addresses a core friction in global trade, where cross-border payments chew up 6-7% in fees annually. Bybit’s model cuts that dramatically, positioning Bybit banking services as a treasury tool for crypto-forward enterprises.

MyBank Business Benefits

-

Streamlined Payroll in 18 fiat currencies like USD and GBP via IBAN accounts for efficient global payments.

-

Instant Hedging enabled by seamless fiat-to-crypto conversions directly on the platform.

-

Reduced FX Fees with low-cost IBAN transfers partnering banks like Pave Bank.

-

Unified KYC for trading and banking, simplifying access despite dual checks with partners.

Accessibility remains gated by regulations. Users in the US or China may face hurdles, as MyBank prioritizes friendly jurisdictions. Full rollout details, including fee structures and yield options on fiat balances, are still forthcoming, but early signals suggest competitive rates to rival traditional savings accounts.

The Road Ahead for Crypto Neobanks

Bybit’s foray signals a broader shift. As exchanges morph into financial hubs, expect more hybrids blending IBANs with DeFi yields. MyBank’s success hinges on user acquisition post-launch; if deposit volumes surge, it validates the neobank play. Watch for integrations like Apple Pay funding or yield-bearing stablecoins, which could elevate it beyond basic transfers. For now, crypto neobank features like these underscore a maturing ecosystem. Bybit users should prepare by completing KYC early, monitoring announcements, and diversifying holdings. This isn’t just about accounts; it’s about owning the full financial stack in a borderless world. Bybit MyBank may not dethrone incumbents overnight, but it carves a compelling niche for those living at the fiat-crypto intersection.

Ultimately, Bybit’s gamble pays off if it delivers the seamlessness promised. In a market chasing the next efficiency leap, MyBank arrives at the right moment, ready to convert skeptics into loyalists.