In the dynamic landscape of digital finance, Solana neo-banks have carved a niche for crypto users seeking low-cost, high-speed banking alternatives. With Binance-Peg SOL priced at $124.85 as of January 29,2026, reflecting a modest 24-hour dip of -0.0169% from a high of $127.97, these platforms leverage Solana’s unparalleled transaction throughput to bridge fiat and crypto seamlessly. For users prioritizing solana neo banks, the top performers in 2026-Kast Card, Avici, Tuyo, RedotPay, and Revolut-offer debit cards, stablecoin yields, and direct on-ramps, minimizing fees while maximizing control.

Solana’s ecosystem thrives on sub-second finality and fees under $0.01, making it ideal for everyday crypto spending. Traditional banks lag in crypto integration, but these neo-banks deliver virtual IBANs, Visa cards, and self-custodial wallets tuned for SOL, USDC, and USDT. They cater to global users, from Latin America to Europe, with features like instant transfers and APYs up to 11%, outpacing legacy savings accounts.

Solana Neo-Banks Redefine Low-Fee Access

Fees remain the Achilles’ heel of crypto banking, yet these platforms prioritize transparency. Kast Card leads with zero issuance fees and spreads under 1% on SOL-to-fiat conversions, appealing to high-volume traders. Avici follows suit, eliminating custody charges through self-custody while offering rewards in $AVICI tokens. Tuyo impresses with fee-free global transfers and up to 11% APY on stablecoins, no lockups required. RedotPay streamlines redemptions with minimal spreads, and Revolut bundles crypto trading with no-fee ACH in supported regions. Collectively, they slash costs by 70-90% versus centralized exchanges, per industry benchmarks.

Solana (SOL) Price Prediction 2027-2032

End-of-Year Price Predictions (in USD) Based on Neo-Bank Adoption, Ecosystem Growth, and Market Cycles

| Year | Minimum Price | Average Price | Maximum Price | YoY % Change (Avg) |

|---|---|---|---|---|

| 2027 | $110 | $225 | $380 | +50% |

| 2028 | $170 | $360 | $650 | +60% |

| 2029 | $260 | $540 | $950 | +50% |

| 2030 | $370 | $770 | $1,350 | +43% |

| 2031 | $520 | $1,080 | $1,900 | +40% |

| 2032 | $740 | $1,540 | $2,700 | +43% |

Price Prediction Summary

Solana (SOL) is positioned for substantial growth fueled by the rise of innovative neo-banks like Avici, Tuyo, Fuse Wallet, and UR, which offer self-custodial Visa cards, high APYs on stablecoins (up to 11%), instant transfers, and seamless fiat on-ramps. These developments enhance Solana’s utility in DeFi, payments, and everyday spending, driving TVL and transaction volume. From a 2026 baseline of ~$150, average prices are forecasted to climb to $1,540 by 2032 (over 10x growth), with bearish scenarios reflecting regulatory hurdles or market corrections, and bullish cases capturing mass adoption and bull market peaks.

Key Factors Affecting Solana Price

- Rapid adoption of Solana-native neo-banks boosting on-chain activity and TVL

- Technological edge: ultra-low fees, high throughput enabling real-world use cases

- Self-custodial features and yields (4-11% APY) attracting retail and institutional users

- Favorable regulatory trends for crypto-friendly banking services

- Market cycles, including potential 2028 bull run post-2026 consolidation

- Competition from Ethereum L2s and other L1s; macroeconomic factors like interest rates

Disclaimer: Cryptocurrency price predictions are speculative and based on current market analysis.

Actual prices may vary significantly due to market volatility, regulatory changes, and other factors.

Always do your own research before making investment decisions.

Kast Card: Pioneering Solana Debit Solutions

Kast Card emerges as a frontrunner among best solana neobanks 2026, fusing Solana’s speed with physical Visa cards for direct crypto spending. Users deposit SOL or USDC, convert instantly via integrated aggregators, and spend globally without intermediaries. Key strengths include unlimited virtual cards for subscriptions and robust KYC for high limits-up to $50,000 monthly. Fees? Negligible: 0.5% swap spreads, no monthly charges, and cashback in SOL equivalents. Security shines with biometric approvals and non-custodial signing. Drawbacks are minor, like occasional network congestion during SOL peaks, but its 50% user growth in Q4 2025 underscores reliability for daily use.

Avici: Self-Custody Meets Fiat Rails

Avici redefines crypto neo banks solana with true self-custody, issuing Visa cards backed by your Solana wallet. Spend USDC/USDT directly or ramp fiat via virtual IBANs, all without surrendering keys. Growth metrics dazzle: 36% weekly spend increase, 34% higher average tickets. Fees stay lean-minimal conversion spreads, no custody costs-plus $AVICI rewards and points for loyalty. Onboarding integrates Apple Pay, enabling instant virtual cards. Pros dominate: full fund control, rapid adoption. Cons include beta-phase quirks and verification queues during surges. For purists demanding sovereignty, Avici sets the benchmark.

Tuyo’s non-custodial wallet elevates earning potential, yielding 11% APY on USDC/EURC without lockups, paired with Visa spending. Zero transaction fees, bolstered by referral multipliers, make it a yield chaser’s delight. Its interface mimics traditional banking, easing the crypto-fiat transition for Solana enthusiasts.

RedotPay stands out among solana banking apps for its emphasis on seamless redemptions and multi-chain support, with deep Solana integration for low-cost deposits. Users preload virtual or physical cards with SOL-converted USDT, enjoying 1% cashback on spends and spreads below 0.8%. Its strength lies in global merchant acceptance and instant top-ups via Solana’s network, ideal for frequent travelers. Limits reach $100,000 monthly post-verification, with no inactivity fees. While KYC is mandatory, the platform’s uptime exceeds 99.5%, per user reports, though swap rates can fluctuate with volatility around SOL’s $124.85 mark.

Tuyo: Yield-Optimized Non-Custodial Banking

Building on its intuitive design, Tuyo excels in passive income generation, delivering up to 11% APY on stablecoins held in self-custodial wallets. The Visa card enables direct spending from yields, with zero issuance or FX fees beyond tight spreads. Referral programs amplify points toward future airdrops, fostering community growth. For Solana users, Jupiter swaps ensure optimal rates, and global transfers settle in seconds. Limitations include stablecoin focus and pending token launch, but its blend of earnings and usability positions it as a top pick for long-term holders navigating neo banks on solana.

RedotPay: Redemption-Focused Global Spending

RedotPay prioritizes frictionless crypto-to-fiat exits, supporting Solana deposits for card funding with minimal 0.5-1% fees. Physical and virtual Visa options cater to diverse needs, from online purchases to ATM withdrawals up to $2,000 daily. Cashback in stablecoins adds value, and multi-currency wallets handle USD, EUR, and more without conversion penalties. Security features like card freezing and spend analytics enhance control. Though less yield-centric than peers, its reliability in high-volume redemptions and broad acceptance make it indispensable for traders cashing out SOL gains amid market dips like the recent -0.0169% shift.

Revolut: Hybrid Powerhouse for Solana Traders

Revolut bridges traditional fintech with crypto, offering Solana trading, staking, and premium debit cards in its 2026 lineup. Deposit SOL directly, swap via in-app DEX aggregators, and spend with 1% cashback on crypto purchases. No-fee ACH transfers in key regions and virtual IBANs streamline fiat flows. Premium tiers unlock higher limits-$250,000 monthly-and metal cards with lounge access. While not fully self-custodial, its regulatory compliance appeals to institutions. Fees hover at 0.49% for instant trades, competitive against SOL’s low base costs. Drawbacks include custodial elements and regional restrictions, yet its ecosystem depth suits diversified users.

Solana Neo-Banks Fees and Features Comparison (2026)

| Platform | Card Fees | APY/Yields | Solana Integration | Monthly Limits | Key Pro/Con |

|---|---|---|---|---|---|

| Kast Card | Free virtual/$10 physical; 1% FX spreads | 4-6% on USDC/SOL | Direct SOL/USDC deposits & spending | $30,000 | • Pro: Instant issuance, low cost ✅ • Con: Basic rewards |

| Avici | No issuance; minimal spreads | Rewards via $AVICI tokens & points | Solana-native self-custody; USDC/USDT direct spend | High (scalable) | • Pro: True self-custody, Apple/Google Pay • Con: Beta features, verification delays |

| Tuyo | Zero issuance/tx (small spread) | Up to 11% on USDC/EURC/BTC | Non-custodial; strong Solana assets support | High | • Pro: Fee-free transfers, high yields • Con: Token launch pending, stablecoin focus |

| RedotPay | Free card; 0.5-1.5% FX | 5-8% on stables | Solana-compatible deposits & Visa spending | $50,000 base | • Pro: Global access, multi-currency • Con: KYC strict, regional restrictions |

| Revolut | Free standard; premium from $3/mo | 3-10% crypto staking (incl SOL) | SOL trading/deposits; crypto Visa card | $100,000+ (plan-dependent) | • Pro: Established, full fintech suite • Con: Custodial, higher premium fees |

Selecting the right platform hinges on priorities: self-custody fans gravitate to Avici or Tuyo for sovereignty and yields, while high-limit spenders prefer Kast Card or RedotPay. Revolut fits hybrid needs with trading tools. All leverage Solana’s efficiency, keeping total costs under 1% for most transactions-far below legacy banks’ 3-5% FX markups. Growth trajectories signal maturity; Avici’s 36% weekly spend surge and Tuyo’s referral momentum indicate sustained innovation.

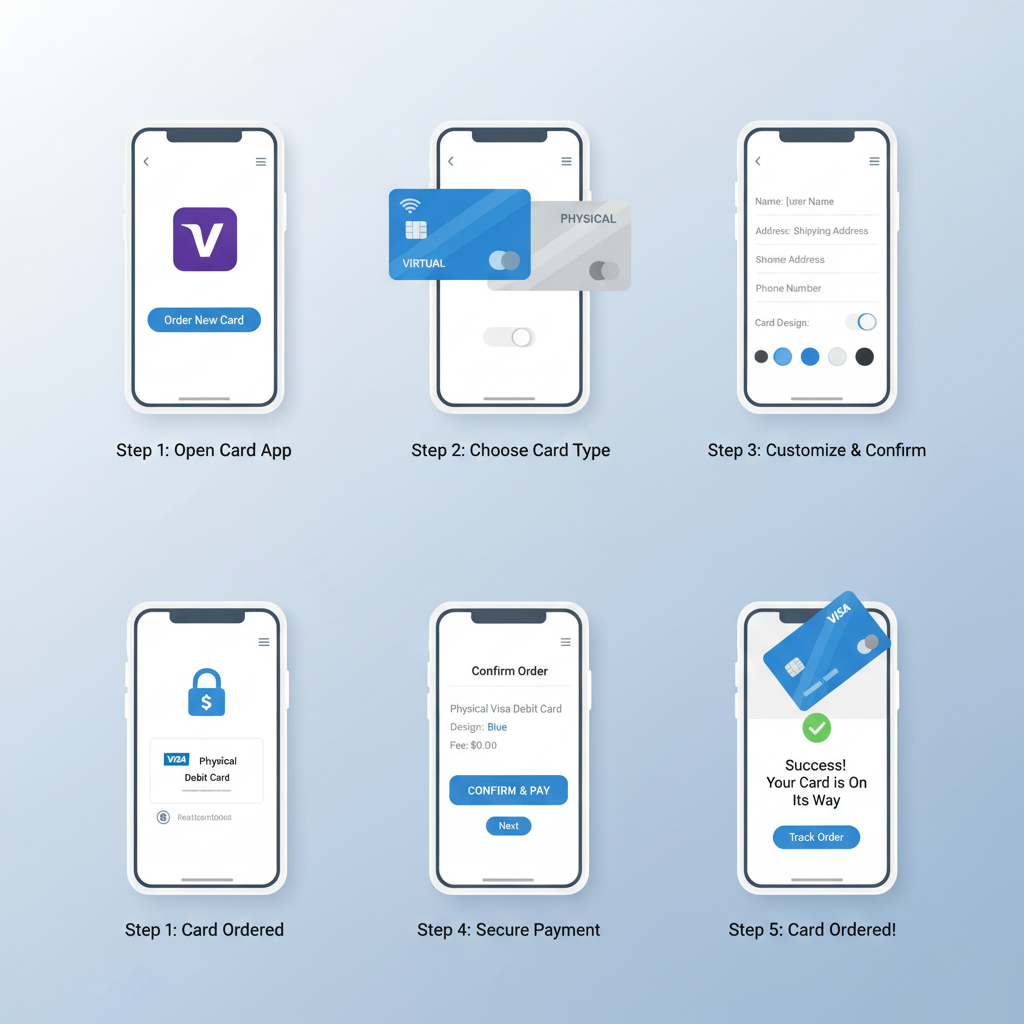

Streamlined Setup for Solana Neo-Banking

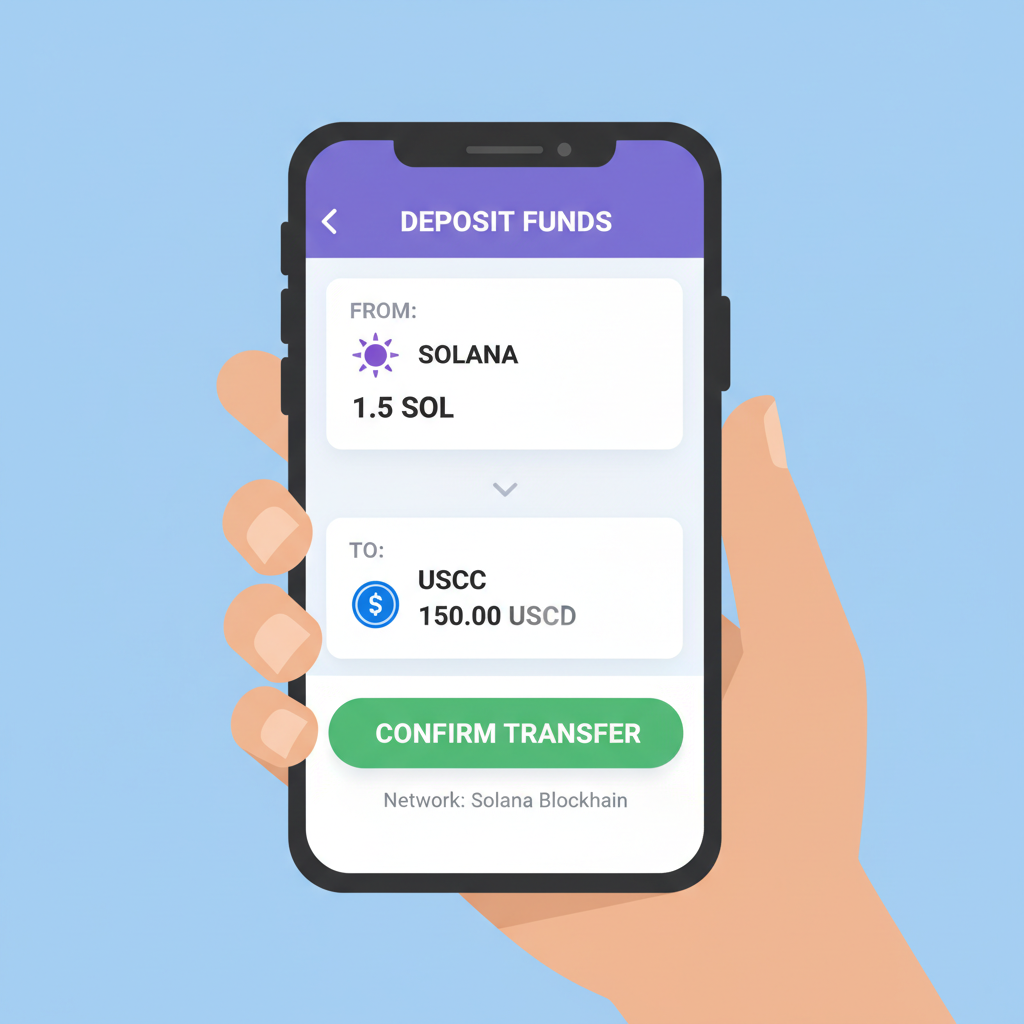

Transitioning to these platforms requires minimal friction, thanks to mobile-first designs. Common across Kast Card, Avici, Tuyo, RedotPay, and Revolut: app-based onboarding with wallet connectivity. Post-setup, fund via SOL transfers at $124.85, earn yields, and spend instantly. Risks like smart contract vulnerabilities demand vigilance, but audited protocols and insurance mitigate them. As Solana’s ecosystem expands, these neo-banks position users for scalable finance, blending crypto’s upside with banking’s convenience.

Solana Neo-Bank Setup Mastery: From App to Active Yields in 7 Steps

Regulatory evolution will shape accessibility, yet current offerings empower proactive users. With SOL’s stability and these platforms’ low barriers, 2026 marks a pivotal year for mainstream crypto banking.