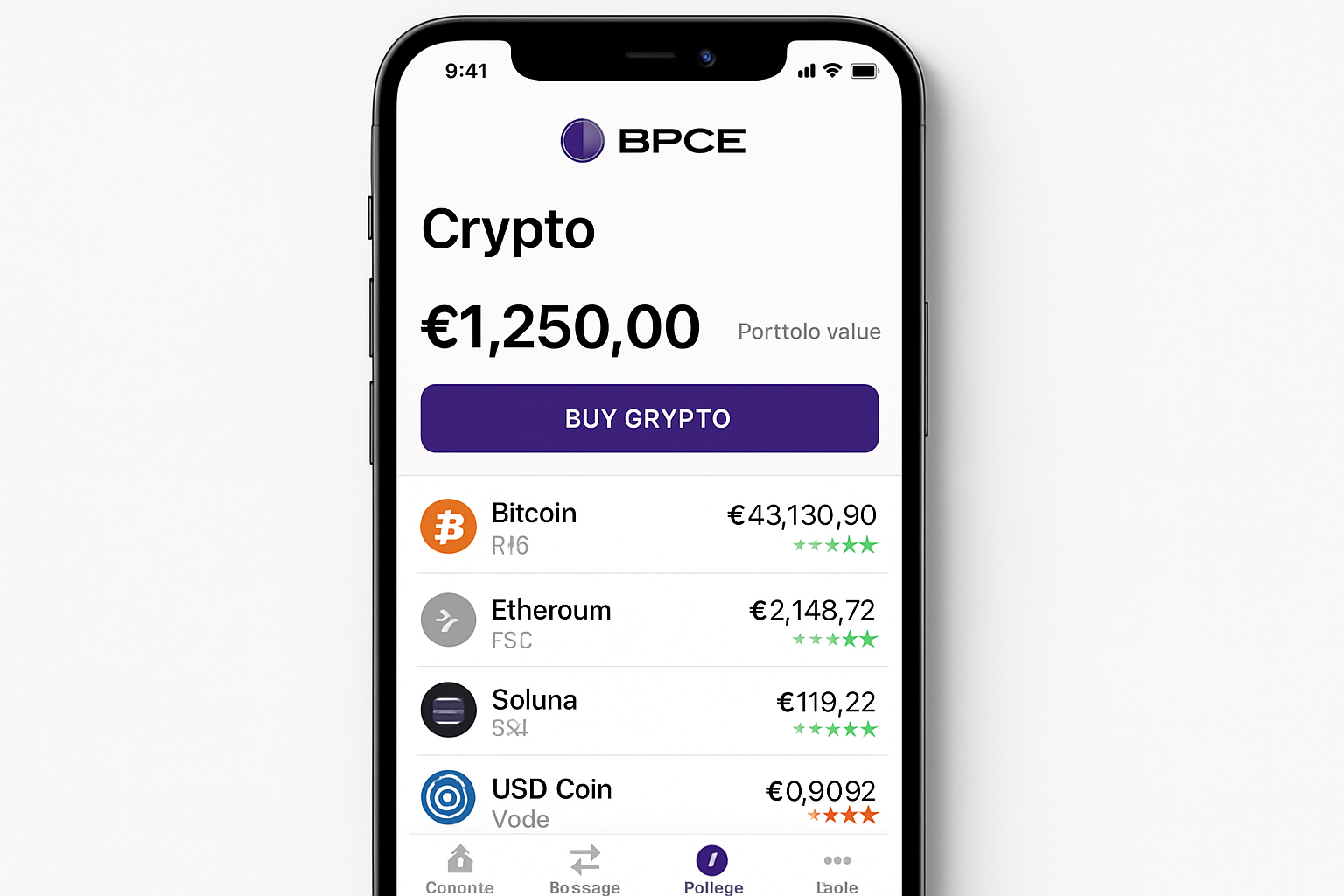

France's second-largest bank just flipped the script on crypto access, rolling out trading services to 2 million customers right inside their mobile apps. BPCE's launch on December 8,2025, marks a massive leap for BPCE crypto trading, blending traditional banking with digital assets in a way that's got the whole industry buzzing. If you're a customer of Banque Populaire Île-de-France or Caisse d'Épargne Provence-Alpes-Côte d'Azur, you're now steps away from buying Bitcoin without leaving your banking app. This phased rollout, powered by BPCE's crypto arm Hexarq, isn't just hype; it's regulated by France's AMF and sets the stage for 12 million users by 2026.

Picture this: no more juggling exchanges or sketchy platforms. BPCE customers dive straight into French bank Bitcoin services with BTC, ETH, SOL, and USDC on tap. Hexarq handles the backend, ensuring compliance and security that rivals any centralized exchange. I've been charting crypto markets for years, and this move screams mainstream adoption. Retail investors who stuck to stocks or savings accounts can now ride crypto volatility from a trusted name, potentially onboarding waves of new money into the space.

Who Gets First Dibs on BPCE's Digital Asset Platform

The initial wave hits four regional banks, serving about 2 million clients under the BPCE 2 million customers crypto banner. That's Banque Populaire Île-de-France, Caisse d'Épargne Provence-Alpes-Côte d'Azur, and two others kicking things off. Eligibility is straightforward: if you're an existing customer in these networks, check your app today. BPCE's strategy here is smart; a controlled launch lets them iron out kinks before scaling nationwide. Data from similar bank integrations, like those in Germany or Switzerland, shows retention spikes when crypto slots into everyday banking. Expect waitlists or quick approvals as demand surges.

This isn't some gimmick. BPCE, with its €1.5 trillion balance sheet, views crypto as the future of finance. Their PSAN license from 2024 gives them the green light, and partnering with Hexarq means robust custody and trading tech. For momentum traders like me, this opens doors for quick BTC swings or SOL plays without cross-border hassles. But let's get real: fees matter, and BPCE's structure is competitive yet transparent.

Fee Breakdown: Is BPCE Crypto Trading Worth the Cost

Transparency is king in crypto services BPCE 2025, and BPCE delivers with clear pricing. No hidden spreads or surprise charges; just a flat monthly account fee and transaction commissions. Here's the data:

BPCE Crypto Fees Table

| Service/Feature | Details |

|---|---|

| Monthly Account Fee | €2.99 |

| Transaction Commission | 1.5% per trade (minimum €1) |

| Supported Assets | BTC, ETH, SOL, USDC |

| Rollout Start | December 8, 2025 |

That €2.99 monthly hit equals about $3.48 USD, pocket change for active traders but a consideration for buy-and-hold folks. The 1.5% commission, with a €1 floor, stacks up well against Binance's spot fees or Coinbase's retail rates, especially sans withdrawal costs since assets stay in-app. Crunch the numbers: on a €1,000 BTC buy, you're out €15 plus the monthly. For high-volume users, negotiate volume discounts might come later, but this baseline screams accessibility. Compared to peers, Société Générale's crypto arm charges steeper, making BPCE a frontrunner in France.

How to Jump In: Your Access Guide to BPCE Crypto Trading

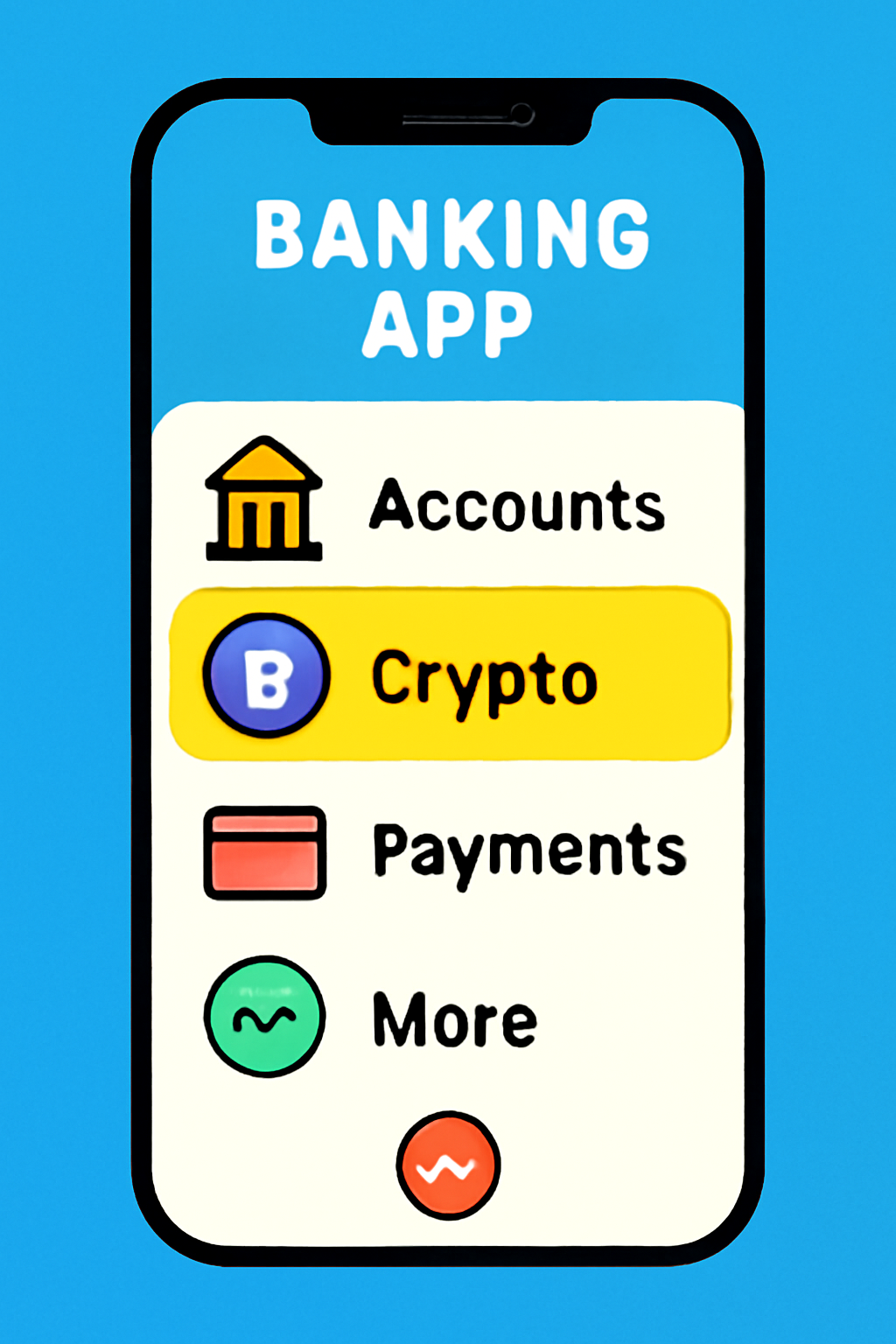

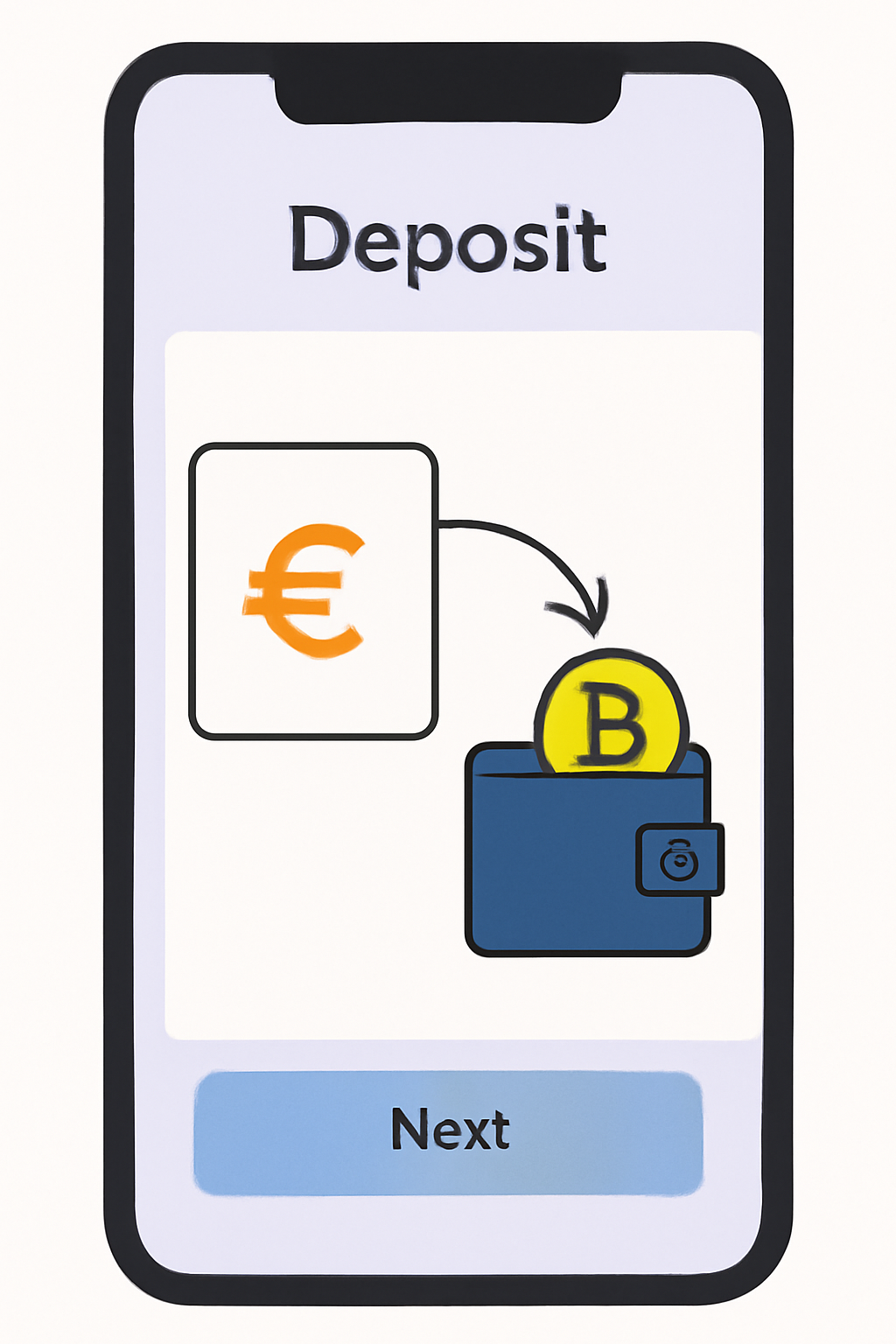

Setting up is dead simple, designed for non-techies dipping into BPCE digital asset platform. Fire up your Banque Populaire or Caisse d'Épargne app, navigate to the new crypto section, and activate a dedicated digital asset account. Verification ties to your existing KYC, so no endless paperwork. Once live, deposit euros instantly from your main account, then buy BTC at market or set limits on ETH dips. Sell anytime, with funds sweeping back to fiat seamlessly.

Pro tip: start small to test the waters. With SOL's speed and USDC's stability, diversify early. BPCE's app integrates charts and alerts, pulling real-time data for informed trades. I've seen banks fumble launches, but BPCE's regional focus minimizes downtime risks. By mid-2026, when all 27 entities join, this could redefine European retail crypto.

One thing that sets BPCE apart in the crowded BPCE digital asset platform space is the seamless integration. No clunky APIs or third-party logins; everything lives under one roof. For traders eyeing SOL's ecosystem plays or ETH's upgrades, this frictionless setup means faster execution during pumps.

🚀 BPCE Crypto Trading: 5 Steps to Start Buying BTC, ETH, SOL & USDC Today!

With that account humming, you're trading in minutes. BPCE's emphasis on user education shines through app tutorials and risk warnings, crucial as volatility hits newcomers hard. I've traded through bank pivots before, and this feels polished from day one.

Security and Compliance: Why BPCE Feels Rock Solid

Hexarq isn't flying blind; their PSAN nod from the AMF in 2024 means full regulatory oversight, cold storage for assets, and insurance against hacks. Think segregated accounts and real-time monitoring, standards that match top exchanges. In a year rife with exchange dramas, BPCE's conservative rollout dodges those pitfalls. Customers get 2FA, biometric logins, and transaction limits for starters. Data backs this: French-regulated platforms saw zero major breaches last year, per AMF reports. For French bank Bitcoin services, it's as safe as your savings account, minus FDIC but with crypto-grade custody.

That said, crypto's wild side demands respect. Leverage? None here, smartly. But market swings can wipe gains quick. BPCE caps exposure per user initially, fostering discipline over FOMO trades.

Head-to-Head: BPCE Fees vs Global Exchanges

To gauge value, let's stack BPCE crypto trading against heavyweights. Their 1.5% commission bites more than Binance's maker-taker tiers under 0.1% for high volume, but BPCE bundles custody and fiat ramps free. Coinbase retail hovers at 1.49% plus spreads, often totaling 2% effective. Revolut's crypto fees? Around 1.5-2%, with worse asset selection. BPCE wins on convenience for casuals, though power users might hybrid with DEXs.

Project monthly costs: €36 yearly fee for light traders, negligible against potential ETH staking yields or BTC appreciation. As volumes climb, expect tiered rebates; BPCE hinted at loyalty perks. This positions them ahead of Boursorama or Credit Agricole, who lag in crypto. Société Générale's Tokenfunder? Enterprise-focused, pricier at 2-3%. BPCE democratizes access, fueling crypto services BPCE 2025 growth.

Market Momentum: 2 Million Users Change the Game

Zoom out: 2 million eyeballs on crypto via BPCE apps could pump €500 million and inflows, based on average retail deposits from similar launches like Deutsche Bank's. BTC liquidity gets a boost, stabilizing French pairs. SOL benefits too, with its DeFi edge drawing yield hunters. USDC shores up stablecoin demand amid MiCA regs. I've charted adoption curves; bank integrations spike volumes 20-30% short-term, per Chainalysis data.

Expansion to 12 million by 2026? That's France's retail crypto gateway, pressuring rivals to match. Europe-wide, it pressures ING or BBVA to accelerate. For momentum plays, watch BTC resistance post-launch; SOL could moon on fresh capital. BPCE isn't just trading; they're wiring traditional wealth into blockchain.

If you're eligible, activate now and snag early positioning. This launch cements France as Europe's crypto hub, blending prudence with innovation. Ride smart, stack sats, and watch banking evolve.

No comments yet. Be the first to share your thoughts!