2024 has been a watershed year for U. S. banks integrating crypto payments. The landscape isn’t just changing – it’s accelerating, as regulatory clarity, competitive pressure, and customer demand converge to bring digital assets into the heart of mainstream banking. If you’re wondering how these seismic shifts impact you as a bank customer or business owner, let’s unpack what’s really happening behind the headlines.

Regulatory Green Lights: The Catalyst for Crypto Banking 2024

Until recently, most U. S. banks tiptoed around crypto services, citing regulatory uncertainty and compliance headaches. That changed in early 2025. The Office of the Comptroller of the Currency (OCC) made waves by confirming national banks could engage in select crypto activities – like crypto-asset custody and stablecoin operations – without jumping through endless regulatory hoops. Meanwhile, the FDIC rescinded its restrictive guidance, giving supervised banks the green light to participate in permissible crypto-related activities without prior approval (see our deep dive on custody and payment integration).

This regulatory shift isn’t just legalese. It means your bank can now offer services like holding your Bitcoin securely or letting you pay vendors with stablecoins, all within the familiar safety net of FDIC oversight. It’s a sharp pivot from the old days of shadowy offshore exchanges and DIY wallets.

Bank Initiatives: From Custody to Crypto Payments

The big players aren’t wasting time. In October 2025, U. S. Bancorp launched a dedicated digital assets unit focused on stablecoin issuance, asset tokenization, and, crucially, crypto payment rails. Citigroup rolled out Citi Token Services, converting deposits into blockchain-based tokens for instant cross-border transfers – a game-changer for businesses tired of waiting days for wires to clear.

Bank of America is exploring its own stablecoin, while PayPal now lets U. S. merchants accept over 100 different cryptocurrencies with lower transaction fees than traditional card networks. Visa and Mastercard have also jumped in, building networks to support stablecoin payments at millions of merchant locations nationwide.

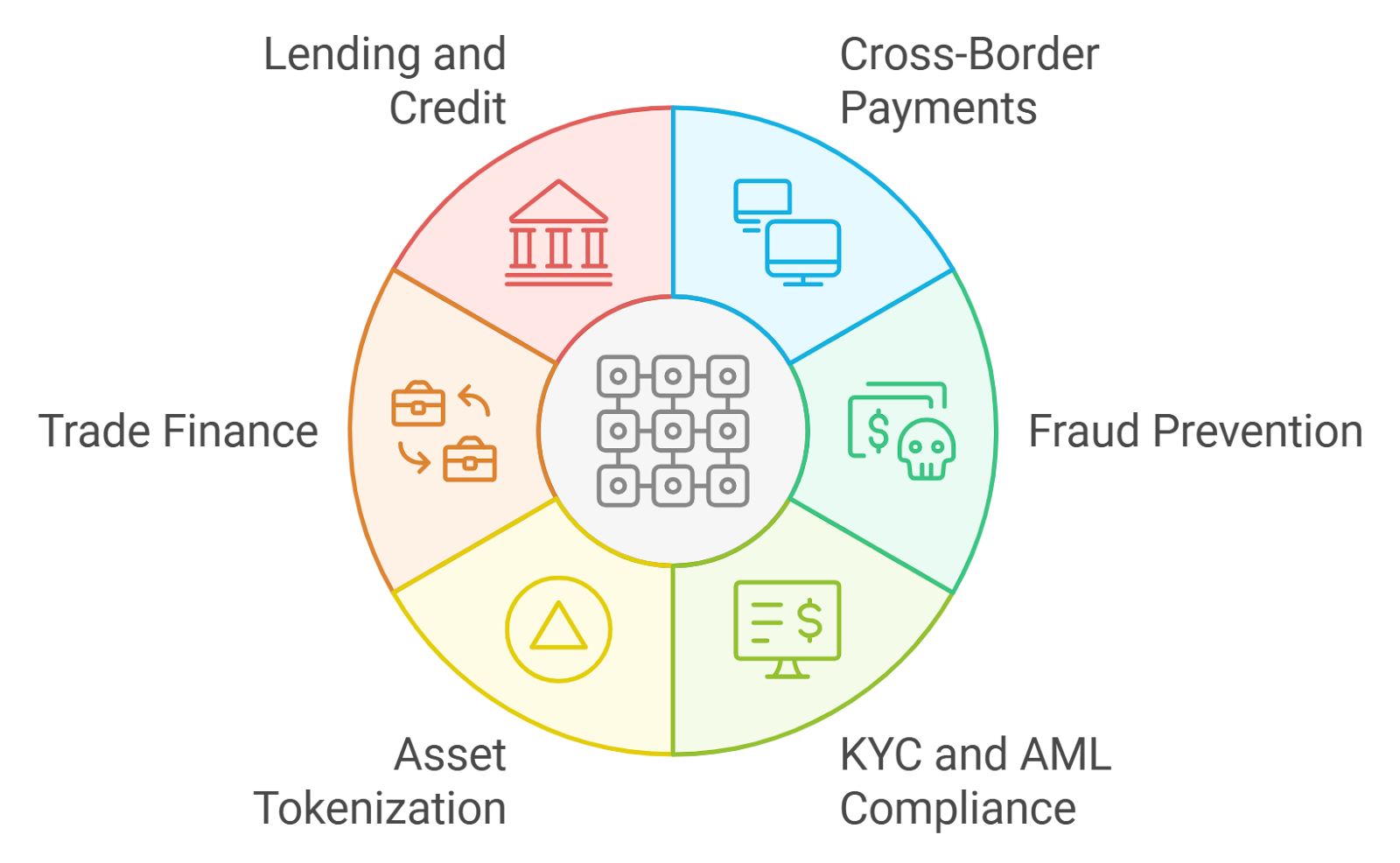

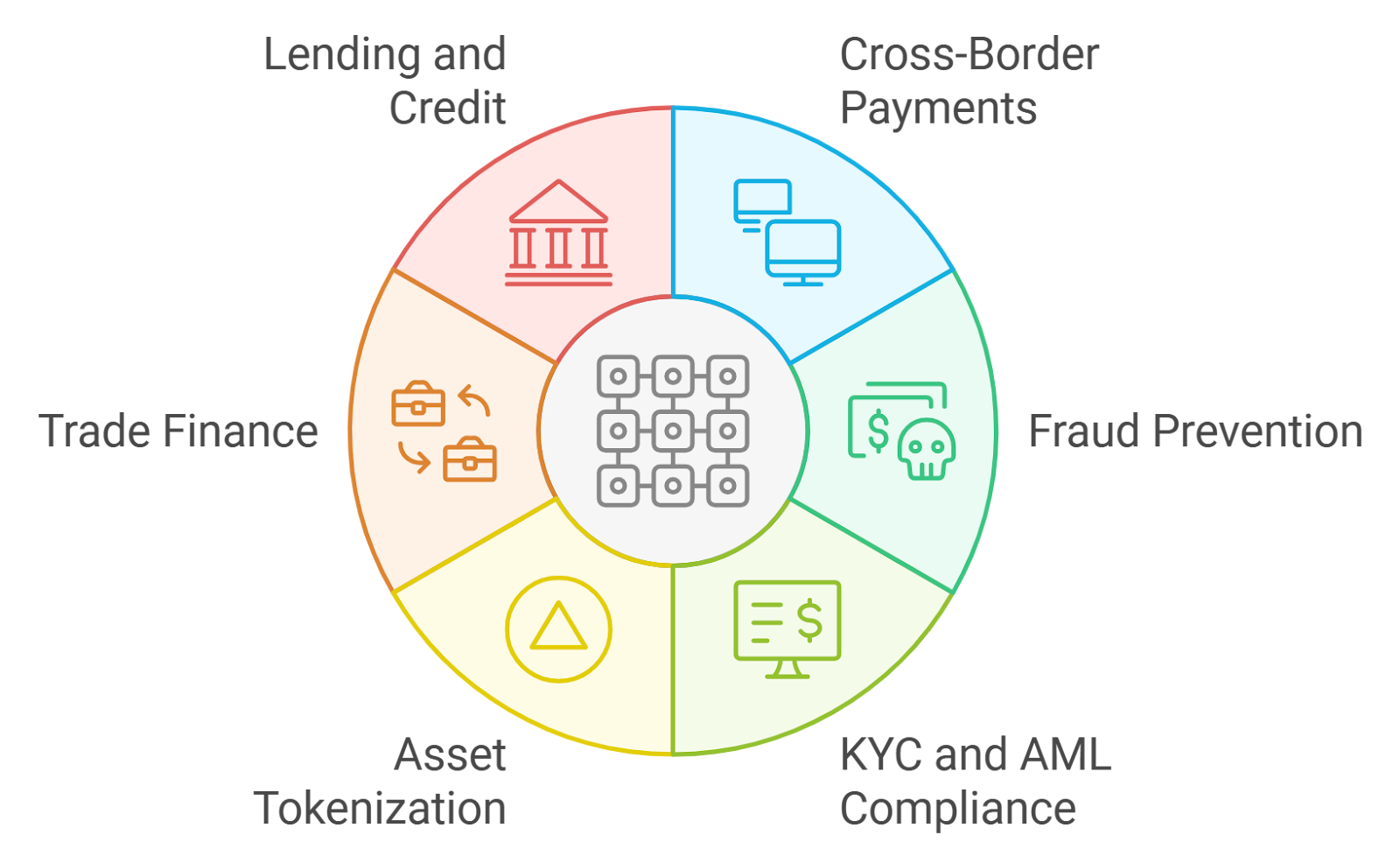

Major U.S. Banks and Their 2024 Crypto Payment Moves

-

U.S. Bank (U.S. Bancorp): In 2024, U.S. Bank resumed cryptocurrency custody services and established a dedicated Digital Assets & Money Movement unit focused on stablecoin issuance, crypto custody, and asset tokenization. This marks a significant commitment to integrating crypto into mainstream banking.

-

Citigroup: Citi launched Citi Token Services, a platform that tokenizes customer deposits for instant blockchain-based cross-border payments. The bank is also exploring a proprietary stablecoin to further streamline digital asset transactions.

-

Bank of America: Bank of America is actively considering the launch of a proprietary stablecoin to facilitate faster and cheaper payments, pending further regulatory clarity and customer demand. The bank is closely monitoring evolving crypto regulations.

-

JPMorgan Chase: JPMorgan continues to expand the use of JPM Coin, its blockchain-based digital currency, for institutional payments and settlements. The bank also leverages its Onyx blockchain platform for cross-border payment innovation.

-

Wells Fargo: Wells Fargo is piloting blockchain-based cross-border payments and exploring stablecoin integration to improve settlement speed and transparency for corporate clients.

It’s not hype – it’s real infrastructure that’s rolling out now. Stablecoin payment volumes alone hit $5.7 trillion in 2024, according to BVNK, and the momentum is only building as banking giants race to capture market share.

What Customers Need to Watch For: Opportunities and Real Risks

This new era brings tangible benefits for customers: faster cross-border transactions, 24/7 settlement, and potentially lower fees for both consumers and merchants. Imagine paying your freelancer in Europe instantly or settling invoices outside business hours – all from your regular bank app.

But there are caveats. Crypto assets remain volatile, and while bank custody offers more security than DIY wallets, you still need to understand the risks around price swings and evolving regulations (get up to speed on new federal rules here). Not every bank is moving at the same pace either; some are still piloting features while others already offer full-service crypto banking.

Another key consideration is user experience. As banks roll out crypto services, integration is everything. The best banks are making crypto payments feel seamless, no need to jump between apps or worry about complex wallet addresses. Instead, you’ll see options like “Pay with Stablecoin” or “Send Crypto” right alongside your traditional payment choices. This is a huge leap for mainstream adoption, putting digital assets on equal footing with dollars and cards.

On the business side, these changes mean more efficient treasury management and new ways to reach global customers. Small businesses, in particular, benefit from faster settlements and reduced reliance on costly intermediaries. U. S. Bank’s new accounts payable platform, for example, is already helping SMBs streamline cash flow with crypto-enabled automation. The days of waiting three business days for international wires? They’re numbered.

Trends Shaping Crypto Banking: What’s Next for 2025?

Looking ahead, expect stablecoins to dominate the next phase of crypto banking. With payment-specific stablecoin transaction volumes reaching $5.7 trillion in 2024, banks are racing to build their own tokens or partner with established issuers. This isn’t just about hype, stablecoins offer the price stability and regulatory clarity that Bitcoin and Ethereum can’t match for day-to-day payments.

We’re also seeing an arms race among payment processors and card networks. Visa’s Bridge platform lets you link your crypto wallet directly to your debit card, while Mastercard’s Multi-Stablecoin Network is onboarding merchants at record pace. The result? Crypto is moving from speculative asset to practical payment tool, with familiar brands leading the charge.

Top Trends in U.S. Banks’ Crypto Payment Integration for 2025

-

Regulatory Green Light for Crypto Activities: In March 2025, the OCC and FDIC clarified that U.S. banks can engage in crypto-asset custody and stablecoin operations without prior regulatory approval, paving the way for broader adoption.

-

Stablecoin Integration by Major Banks: Citigroup launched Citi Token Services for instant blockchain-based payments and is exploring a proprietary stablecoin. Bank of America is also considering launching its own stablecoin, reflecting a growing trend among top U.S. lenders.

-

Dedicated Digital Asset Units: U.S. Bancorp established a specialized unit focused on digital assets, stablecoin issuance, and cryptocurrency custody, signaling a strategic commitment to crypto innovation.

-

Expanded Crypto Payment Options for Merchants: PayPal now allows U.S. merchants to accept payments in over 100 cryptocurrencies via its Pay with Crypto platform, offering lower fees and seamless wallet integration.

-

Card Networks Embrace Stablecoins: Visa and Mastercard have launched initiatives to accept stablecoins through platforms like Visa Bridge and Mastercard Multi-Stablecoin Network, enabling millions of merchants to accept crypto payments.

-

Faster, Cheaper Cross-Border Payments: Blockchain and stablecoin adoption by banks like Citigroup is enabling instant, low-cost cross-border transactions, benefiting both businesses and consumers.

-

Greater Consumer Choice and Convenience: With mainstream banks and payment processors integrating crypto, customers can use digital assets for everyday transactions, enjoy faster settlements, and benefit from potentially lower fees.

How to Take Advantage: Smart Moves for Customers

If you want to make the most of this shift, start by checking what your current bank offers, or plans to offer, in terms of crypto services. Some banks provide robust custody and payment options today; others are still in the sandbox phase. Don’t be afraid to shop around or even open a dedicated crypto-friendly account if your main bank is lagging behind (see our step-by-step guide here).

Stay informed about fees. While many banks tout lower transaction costs for crypto payments, fee structures can vary widely between providers, and between types of digital assets. Always read the fine print before moving significant sums.

Monitor regulatory updates. The rules are evolving fast, especially as federal agencies like the OCC and FDIC fine-tune their approach. Bookmark our coverage on emerging trends in licensed crypto banking for the latest insights.

The bottom line: Crypto payment integration is no longer a distant promise, it’s happening right now inside the biggest U. S. banks. Whether you’re eager to pay with stablecoins, streamline business operations, or simply diversify your holdings with institutional-grade security, 2024,2025 is your window to get ahead of the curve.