In 2025, the digital banking sector is witnessing a seismic shift as on-chain neo banks emerge at the intersection of blockchain innovation and mainstream finance. These new-age platforms, built natively on blockchain infrastructure and powered by stablecoins, are challenging the very definition of what it means to be a bank in the digital era. The launch of Plasma One, the world’s first stablecoin-native neobank, is emblematic of this transformation and signals a new chapter for both retail and institutional users seeking borderless, efficient financial solutions.

Plasma One: A Glimpse Into Stablecoin-Native Banking

Plasma One, launched in September 2025 by Milan-based Plasma, is designed from the ground up for stablecoin users. Unlike legacy digital banks that retro-fit crypto functionality onto traditional rails, Plasma One operates entirely on-chain. Its core offerings include:

- One-click fiat gateways: Users can instantly deposit or withdraw funds via local cash networks, removing friction between digital assets and real-world spending.

- Proprietary payment stack: Built atop Plasma’s in-house blockchain, transactions settle in under two seconds, dramatically improving speed for global transfers.

- Rewards-driven card payments: Cardholders receive cashback incentives for using stablecoins in everyday purchases, driving adoption among both crypto-natives and newcomers.

This holistic approach addresses persistent pain points, such as clunky interfaces and limited cash-out options, that have historically hampered stablecoin usability. The result? A platform aiming to make saving, spending, and earning in digital dollars as seamless as using any mainstream fintech app.

The Mainstreaming of Stablecoins: Traditional Banks Take Notice

The disruptive potential of stablecoin-native banking has not gone unnoticed by legacy financial giants. In July 2025, Citigroup’s CEO Jane Fraser publicly confirmed that Citi is considering launching its own stablecoin to stay ahead in digital payments innovation (source). Bank of America has announced similar ambitions, with CEO Brian Moynihan highlighting ongoing internal development efforts. Morgan Stanley’s leadership has also acknowledged the strategic importance of stablecoins for future operations, though with cautious optimism as they continue to assess applicability (source).

This convergence marks a pivotal moment: traditional banks are no longer mere observers but active participants in shaping the next phase of blockchain digital banking. Their entry brings additional credibility, and regulatory scrutiny, to the sector while accelerating innovation around cross-border payments and treasury management.

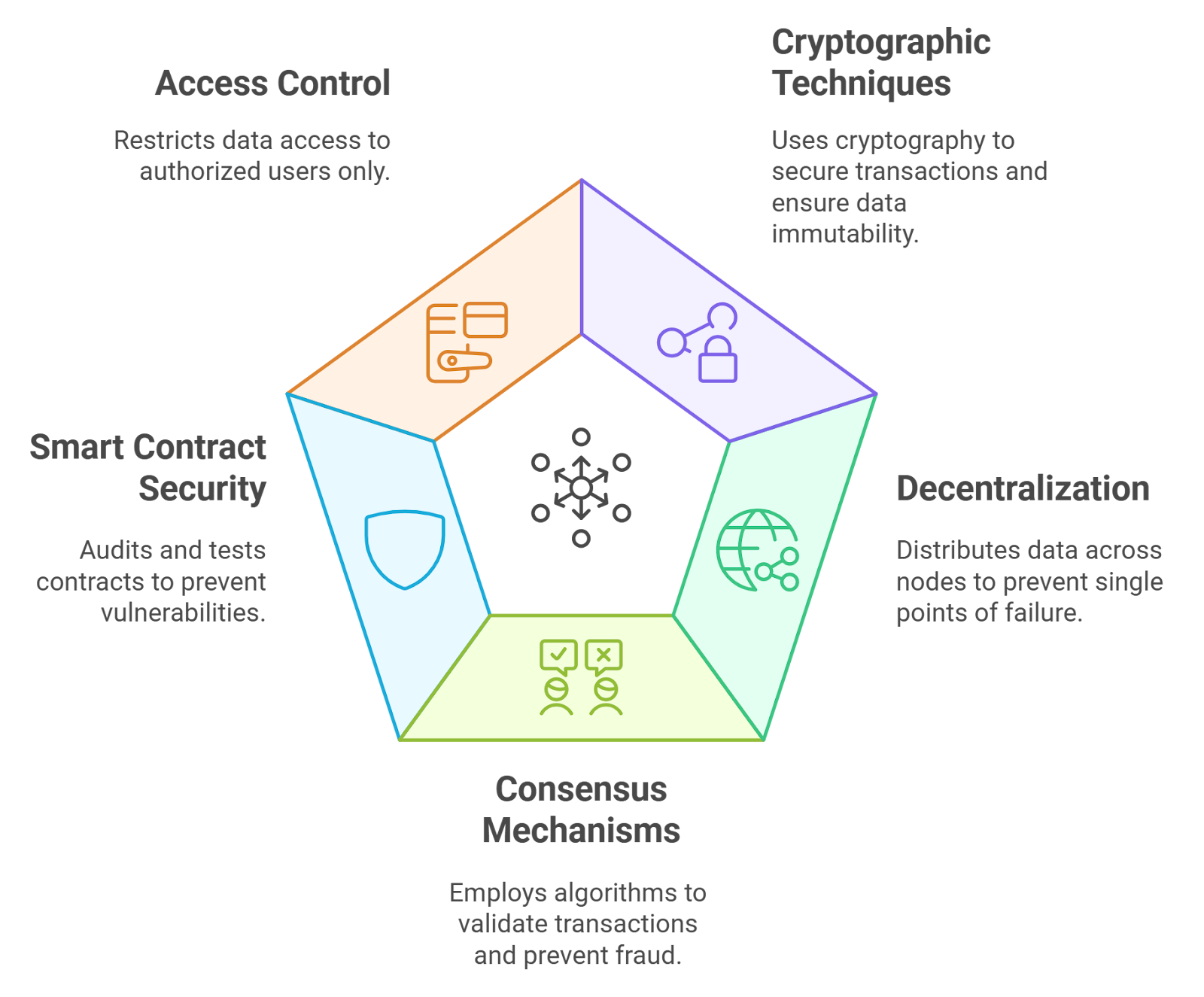

Key Advantages of On-Chain Neo Banks in 2025

-

Instant, Low-Cost Transactions: On-chain neo banks like Plasma One leverage proprietary blockchain payment stacks, enabling transactions to settle in under two seconds and at a fraction of traditional banking fees.

-

Global, 24/7 Access Without Borders: Operating entirely on blockchain, stablecoin-native platforms provide uninterrupted banking services worldwide, removing barriers imposed by national banking hours or local infrastructure.

-

Seamless Fiat On/Off Ramps: Platforms such as Plasma One offer one-click fiat gateways, allowing users to instantly deposit or withdraw funds through local cash networks—streamlining the conversion between digital dollars and local currencies.

-

Enhanced Financial Inclusion: By utilizing stablecoins, on-chain neo banks reach underserved populations in emerging markets, offering permissionless access to saving, spending, and earning in digital dollars.

-

Rewards-Driven Payments: Innovative features like rewards-driven card payments (e.g., cashback incentives on Plasma One) encourage adoption and provide tangible benefits for users transacting in stablecoins.

-

Transparency and Security: All transactions are recorded on public blockchains, providing auditable, tamper-resistant records and reducing the risk of fraud compared to traditional digital banks.

-

Programmable Financial Services: Smart contracts enable automated, customizable financial products—such as savings, lending, and payments—without intermediaries, increasing efficiency and reducing operational risks.

The Visa Effect: Stablecoins Accelerate Global Payments

If there was any doubt about the mainstream viability of stablecoins, Visa’s latest pilot program puts those concerns to rest. In September 2025, Visa began testing international payments using pre-funded stablecoins rather than conventional fiat currencies (source). This move enables businesses to settle transactions faster while freeing up working capital previously locked across multiple currencies worldwide, a game-changer for global commerce.

The implications extend beyond convenience; they signal a broader acceptance that blockchain-based money can deliver real-world efficiency gains at scale. As more payment networks integrate with on-chain protocols and USDT neo banks or SOL stablecoin banks gain traction, expect cross-border settlements to become near-instantaneous, a far cry from today’s multi-day SWIFT wires or expensive remittance corridors.

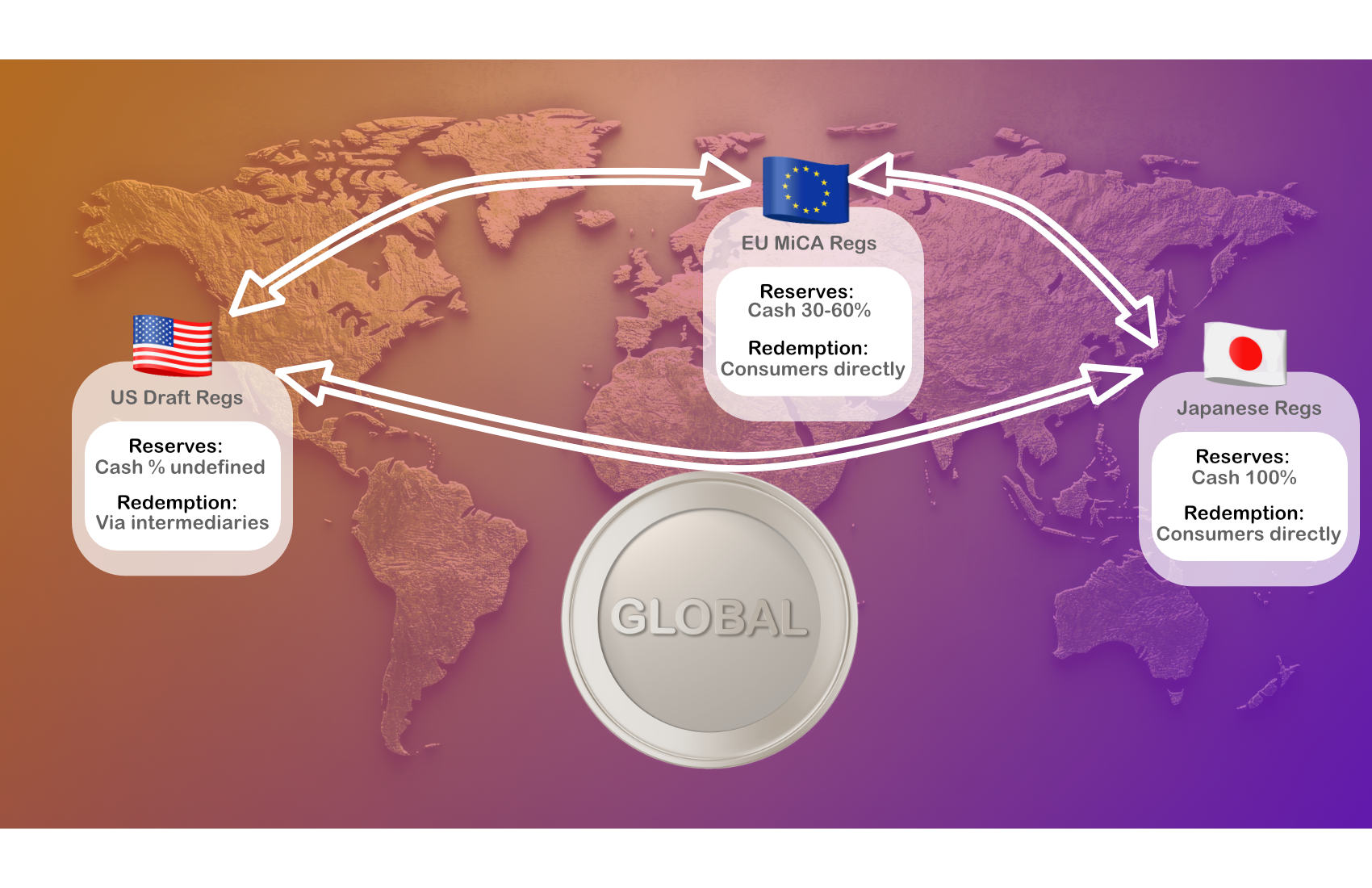

Meanwhile, the regulatory environment is rapidly evolving to support this new paradigm. The passage of the Genius Act in the U. S. provides much-needed legal clarity for stablecoin issuers and on-chain neo banks, laying a foundation for responsible growth and institutional adoption. This clarity is catalyzing further investment and innovation by reducing risk for both startups and established players.

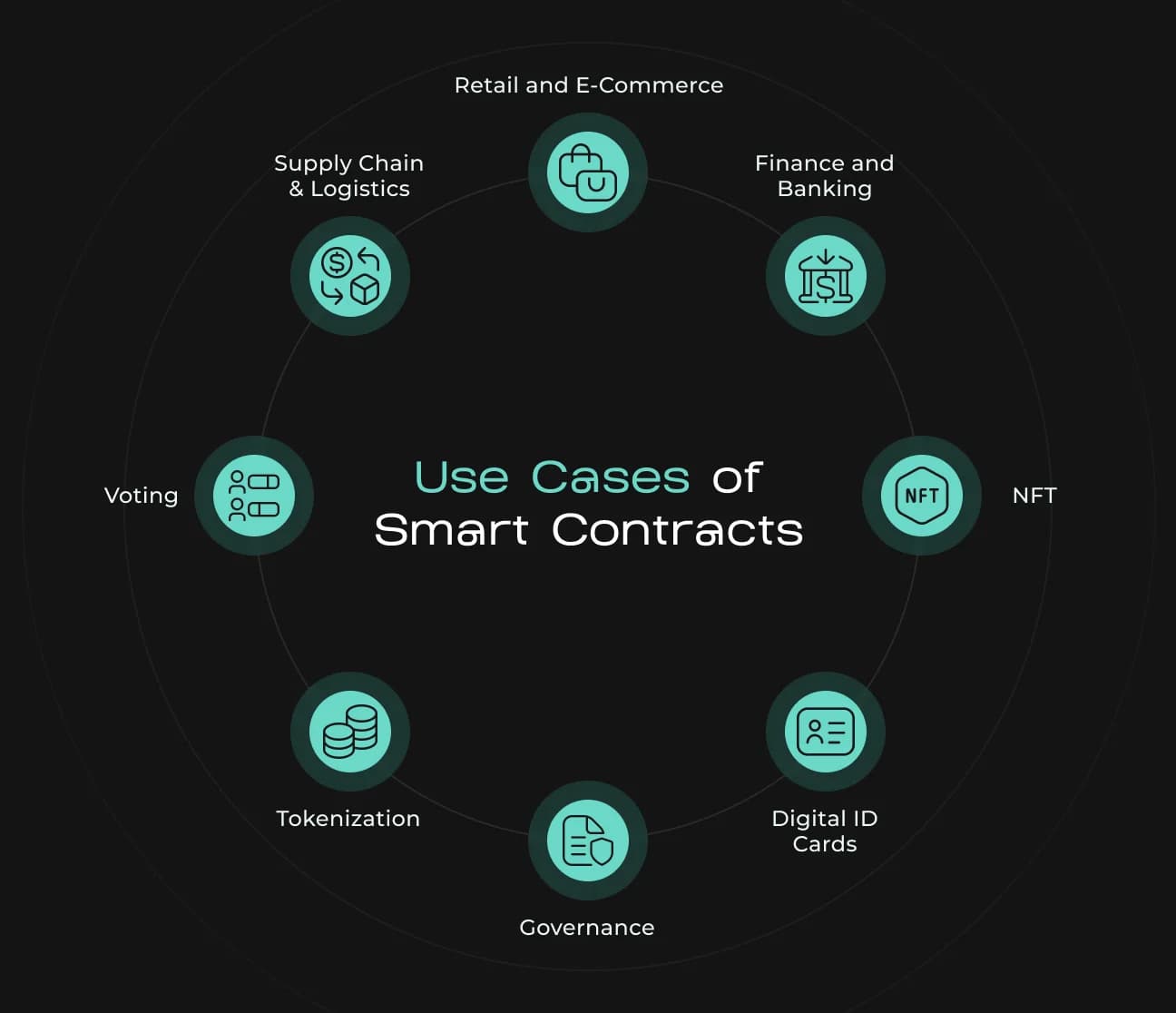

Emerging Use Cases: Stablecoins Power DeFi-Integrated Banking

What truly sets stablecoin-native platforms apart in 2025 is their seamless integration with decentralized finance (DeFi). By leveraging smart contracts, users can access permissionless lending, yield products, and automated savings directly from their banking interface, no separate wallet or technical know-how required. This convergence unlocks new avenues for financial empowerment, especially in regions with limited legacy banking infrastructure.

For example, Plasma One’s app enables users to allocate portions of their stablecoin balance into on-chain savings vaults or participate in liquidity pools with a single tap. These features transform passive account balances into productive assets, democratizing access to yields that were once reserved for sophisticated crypto investors.

Additionally, non-custodial models are gaining traction among privacy-conscious users. Platforms like Plasma One offer options for self-custody or hybrid custody solutions, giving clients full control over private keys while still enjoying the convenience of modern banking UX. This flexibility appeals to both crypto veterans seeking autonomy and newcomers prioritizing ease of use.

Challenges Ahead: Security, Interoperability and User Education

Despite rapid progress, several hurdles remain before stablecoin-native banking reaches mass adoption. Security remains paramount; robust smart contract audits and transparent risk disclosures are essential as more value flows on-chain. Interoperability between chains (e. g. , USDT neo banks on Ethereum vs SOL stablecoin banks on Solana) is another pain point, users expect seamless transfers across networks without technical friction.

User education is equally critical. For many first-time adopters in emerging markets, concepts like private key management or DeFi yield strategies are foreign territory. Leading platforms are investing heavily in intuitive onboarding flows, localized support, and educational content to bridge this gap.

What’s Next? The Roadmap for Crypto Neo Banks in 2025

The next wave of innovation will likely focus on three fronts: sustainability (with green blockchain protocols), advanced identity solutions for compliance without sacrificing privacy, and deeper integration with global payment rails. As competition intensifies between pure-play crypto neo banks and incumbent financial giants launching their own stablecoins, end-users stand to benefit from lower fees, faster settlements, and broader financial inclusion.

Top Trends in Stablecoin-Native Banking for 2025

-

On-Chain Neobanks Go Mainstream: The launch of Plasma One marks the rise of neobanks operating entirely on blockchain and stablecoins, offering seamless saving, spending, and earning in digital dollars—especially for emerging markets.

-

Traditional Banks Embrace Stablecoins: Major institutions like Citigroup, Bank of America, and Morgan Stanley are actively exploring or developing stablecoin initiatives, signaling a shift toward integrating digital assets into mainstream banking.

-

Visa Integrates Stablecoins for Payments: Visa is piloting stablecoin-powered international payments, enabling businesses to pre-fund transactions with digital tokens and accelerating cross-border settlements.

-

Regulatory Clarity Spurs Innovation: The passage of the Genius Act in the U.S. provides a clear regulatory framework for stablecoin issuers, boosting institutional confidence and paving the way for broader adoption.

-

Faster, More Accessible Global Finance: Stablecoin-native platforms are reducing transaction times to seconds and lowering costs, making global financial services more accessible and efficient for users worldwide.

The emergence of platforms like Plasma One signals that stablecoin rewards banking, DeFi integration, and instant cross-border payments aren’t just buzzwords, they’re becoming baseline expectations for digital finance in 2025. As regulatory frameworks mature and user experience improves across USDT neo bank apps and SOL stablecoin bank solutions alike, we’re witnessing the dawn of a truly global digital banking ecosystem built natively on blockchain rails.