More Stories

Crypto Bank Comparisons

Crypto-Friendly Banks for Seamless Off-Ramps: Mercury, Tower Bank and Revolut Compared 2026

Bitcoin's grip at $70,850 underscores the urgency for reliable off-ramps in 2026. Traders and businesses need banks that handle crypto-to-fiat conversions without freezes or delays. Enter Mercury, Tower Bank, and Revolut: three powerhouses...

Read More

Crypto Bank Comparisons

Crypto-Friendly Banks for Seamless Off-Ramps: Mercury, Tower Bank and Revolut Compared 2026

Bitcoin's grip at $70,850 underscores the urgency for reliable off-ramps in 2026. Traders and businesses need banks that handle crypto-to-fiat conversions without freezes or delays. Enter Mercury, Tower Bank, and Revolut: three powerhouses...

Read More

Crypto Bank Comparisons

Top On-Chain Crypto Neobanks 2026: Managing Bank-Scale Assets Without Branches

In 2026, the financial world witnesses a seismic shift as on-chain crypto neobanks command billions in total value locked, rivaling traditional banks without a single brick-and-mortar branch. Platforms like Aave and Sky (formerly MakerDAO)...

Read More

Crypto Bank Comparisons

Top On-Chain Crypto Neobanks 2026: Managing Bank-Scale Assets Without Branches

In 2026, the financial world witnesses a seismic shift as on-chain crypto neobanks command billions in total value locked, rivaling traditional banks without a single brick-and-mortar branch. Platforms like Aave and Sky (formerly MakerDAO)...

Read More

Crypto Bank Regulations & Security

Crypto.com U.S. Crypto Bank Charter Approval 2026: Services Fees Security Guide

Crypto. com just notched a massive win in the U. S. regulatory arena, securing conditional approval from the OCC for its national trust bank charter on February 23,2026. This positions the exchange as a frontrunner in Crypto. com US crypto...

Read More

Crypto Bank Regulations & Security

Crypto.com U.S. Crypto Bank Charter Approval 2026: Services Fees Security Guide

Crypto. com just notched a massive win in the U. S. regulatory arena, securing conditional approval from the OCC for its national trust bank charter on February 23,2026. This positions the exchange as a frontrunner in Crypto. com US crypto...

Read More

Crypto Bank Regulations & Security

Crypto.com National Trust Bank Charter Approval: Services and Implications for Crypto Users

Exciting times for crypto enthusiasts: Crypto. com just scored conditional approval from the U. S. Office of the Comptroller of the Currency (OCC) to launch Foris Dax National Trust Bank, operating as Crypto. com National Trust Bank ....

Read More

Crypto Bank Regulations & Security

Crypto.com National Trust Bank Charter Approval: Services and Implications for Crypto Users

Exciting times for crypto enthusiasts: Crypto. com just scored conditional approval from the U. S. Office of the Comptroller of the Currency (OCC) to launch Foris Dax National Trust Bank, operating as Crypto. com National Trust Bank ....

Read More

Crypto Banking Guides

On-Chain Crypto Neobanks Managing Billions Without Branches: 2026 Guide

Imagine banking where your money works 24/7 on blockchain rails, no branches, no middlemen, just pure efficiency handling billions in assets. That's the reality of on-chain crypto neobanks in 2026, flipping traditional finance on its head....

Read More

Crypto Banking Guides

On-Chain Crypto Neobanks Managing Billions Without Branches: 2026 Guide

Imagine banking where your money works 24/7 on blockchain rails, no branches, no middlemen, just pure efficiency handling billions in assets. That's the reality of on-chain crypto neobanks in 2026, flipping traditional finance on its head....

Read More

Crypto Bank Reviews

PNC Bank Coinbase Partnership: Bitcoin Ethereum Trading Storage for High-Net-Worth Clients

In the evolving landscape of digital finance, PNC Bank's partnership with Coinbase marks a pivotal shift, enabling high-net-worth clients to trade Bitcoin directly through their traditional banking interface. Launched in December 2025,...

Read More

Crypto Bank Reviews

PNC Bank Coinbase Partnership: Bitcoin Ethereum Trading Storage for High-Net-Worth Clients

In the evolving landscape of digital finance, PNC Bank's partnership with Coinbase marks a pivotal shift, enabling high-net-worth clients to trade Bitcoin directly through their traditional banking interface. Launched in December 2025,...

Read More

Crypto Bank Reviews

Crypto Banks Offering Stablecoin Wallets: Top Picks for Secure Integration in 2026

In 2026, stablecoins are no longer just a DeFi darling; they're the backbone of everyday digital transactions, offering the stability of fiat with the speed of blockchain. If you're tired of volatile crypto swings derailing your plans,...

Read More

Crypto Bank Reviews

Crypto Banks Offering Stablecoin Wallets: Top Picks for Secure Integration in 2026

In 2026, stablecoins are no longer just a DeFi darling; they're the backbone of everyday digital transactions, offering the stability of fiat with the speed of blockchain. If you're tired of volatile crypto swings derailing your plans,...

Read More

Crypto Bank Comparisons

Crypto Banks High Yield Savings Accounts vs Traditional Banks 2026 Comparison

In February 2026, the savings landscape splits sharply between traditional banks offering steady 4-5% APY with full FDIC protection up to $250,000 and crypto platforms pushing 8-16% yields through lending, staking, and DeFi. Traditional...

Read More

Crypto Bank Comparisons

Crypto Banks High Yield Savings Accounts vs Traditional Banks 2026 Comparison

In February 2026, the savings landscape splits sharply between traditional banks offering steady 4-5% APY with full FDIC protection up to $250,000 and crypto platforms pushing 8-16% yields through lending, staking, and DeFi. Traditional...

Read More

Crypto Bank Regulations & Security

Telcoin Digital Asset Bank Review: Custody Services, Security, and BlackRock Integration 2026

Telcoin Digital Asset Bank just made history as the first federally-regulated digital asset depository institution in the US, headquartered in Norfolk, Nebraska. With final charter approval from the Nebraska Department of Banking and...

Read More

Crypto Bank Regulations & Security

Telcoin Digital Asset Bank Review: Custody Services, Security, and BlackRock Integration 2026

Telcoin Digital Asset Bank just made history as the first federally-regulated digital asset depository institution in the US, headquartered in Norfolk, Nebraska. With final charter approval from the Nebraska Department of Banking and...

Read More

Crypto Bank Reviews

ChainBank Review 2026: USDT USDC Yields and Tokenized RWA Services for Crypto Users

ChainBank is charging ahead in 2026 as the crypto neobank USDT and USDC holders crave for reliable yields. Depositing stablecoins here unlocks passive income through tokenized U. S. Treasury bills, with reserves transparent on-chain. As...

Read More

Crypto Bank Reviews

ChainBank Review 2026: USDT USDC Yields and Tokenized RWA Services for Crypto Users

ChainBank is charging ahead in 2026 as the crypto neobank USDT and USDC holders crave for reliable yields. Depositing stablecoins here unlocks passive income through tokenized U. S. Treasury bills, with reserves transparent on-chain. As...

Read More

Crypto Bank Regulations & Security

Crypto Banks with IBAN Accounts and Yield Earnings: Top 5 Options for Secure Digital Banking in 2026

In the fast-evolving world of digital finance, crypto banks with IBAN accounts and yield earnings stand out as a pragmatic bridge between traditional banking and blockchain innovation. As we hit 2026, investors and businesses demand more...

Read More

Crypto Bank Regulations & Security

Crypto Banks with IBAN Accounts and Yield Earnings: Top 5 Options for Secure Digital Banking in 2026

In the fast-evolving world of digital finance, crypto banks with IBAN accounts and yield earnings stand out as a pragmatic bridge between traditional banking and blockchain innovation. As we hit 2026, investors and businesses demand more...

Read More

Crypto Bank Regulations & Security

Fasset Crypto Bank Review: Licensed Platform for Tokenized RWAs and Borderless Transfers 2026

In the fast-evolving world of crypto banking, Fasset stands out as a licensed powerhouse blending Shariah-compliant principles with tokenized real-world assets (RWAs) and seamless borderless transfers. As we hit 2026, this Fasset crypto...

Read More

Crypto Bank Regulations & Security

Fasset Crypto Bank Review: Licensed Platform for Tokenized RWAs and Borderless Transfers 2026

In the fast-evolving world of crypto banking, Fasset stands out as a licensed powerhouse blending Shariah-compliant principles with tokenized real-world assets (RWAs) and seamless borderless transfers. As we hit 2026, this Fasset crypto...

Read More

Crypto Banking Products & Services

On-Chain Neobanks Managing Billions in Crypto Assets Without Branches 2026

As Bitcoin holds steady at $69,615.00 , up $2,819.00 over the past 24 hours with a high of $69,821.00 and low of $66,780.00, the crypto landscape in early 2026 reveals a maturing ecosystem where volatility meets innovation. On-chain...

Read More

Crypto Banking Products & Services

On-Chain Neobanks Managing Billions in Crypto Assets Without Branches 2026

As Bitcoin holds steady at $69,615.00 , up $2,819.00 over the past 24 hours with a high of $69,821.00 and low of $66,780.00, the crypto landscape in early 2026 reveals a maturing ecosystem where volatility meets innovation. On-chain...

Read More

Crypto Bank Comparisons

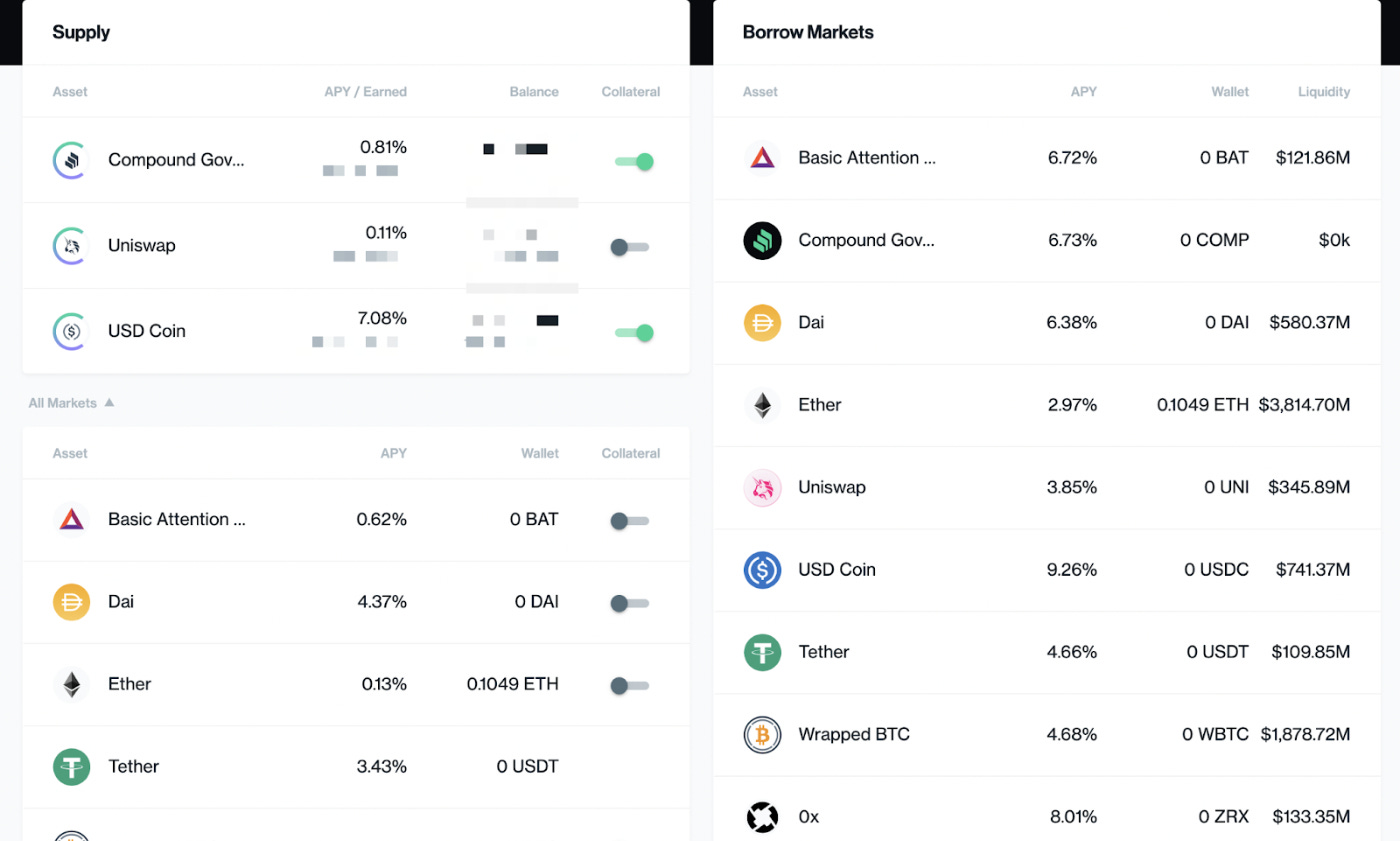

Top On-Chain Crypto Neobanks 2026: Managing Billions in Assets Without Branches

In the dynamic landscape of 2026, on-chain crypto neobanks have redefined financial services by managing billions in assets through decentralized protocols, eliminating the need for physical branches. Platforms like Aave, Morpho, and...

Read More

Crypto Bank Comparisons

Top On-Chain Crypto Neobanks 2026: Managing Billions in Assets Without Branches

In the dynamic landscape of 2026, on-chain crypto neobanks have redefined financial services by managing billions in assets through decentralized protocols, eliminating the need for physical branches. Platforms like Aave, Morpho, and...

Read More

Crypto Bank Reviews

Fasset DeFi Neobank Review: USDC Debit Cards, RWA Investments and Global Payments for Crypto Holders

In the crowded field of crypto neobanks, Fasset emerges as a thoughtful fusion of DeFi innovation and practical banking, tailored for holders seeking stability amid volatility. As a regulated on-chain platform, it bridges the gap between...

Read More

Crypto Bank Reviews

Fasset DeFi Neobank Review: USDC Debit Cards, RWA Investments and Global Payments for Crypto Holders

In the crowded field of crypto neobanks, Fasset emerges as a thoughtful fusion of DeFi innovation and practical banking, tailored for holders seeking stability amid volatility. As a regulated on-chain platform, it bridges the gap between...

Read More

Crypto Bank Reviews

Fasset DeFi Neobank Review: Hold USDC, Invest in RWAs and Use Crypto Debit Cards 2026

In the fast-evolving world of 2026 DeFi neobanks, Fasset cuts through the noise as Indonesia's only licensed powerhouse, blending stablecoin stability with real-world asset (RWA) investments and slick crypto debit cards. Picture this:...

Read More

Crypto Bank Reviews

Fasset DeFi Neobank Review: Hold USDC, Invest in RWAs and Use Crypto Debit Cards 2026

In the fast-evolving world of 2026 DeFi neobanks, Fasset cuts through the noise as Indonesia's only licensed powerhouse, blending stablecoin stability with real-world asset (RWA) investments and slick crypto debit cards. Picture this:...

Read More