In the fast-evolving world of crypto banking, Fasset stands out as a licensed powerhouse blending Shariah-compliant principles with tokenized real-world assets (RWAs) and seamless borderless transfers. As we hit 2026, this Fasset crypto bank is no longer just a promise; it's delivering on financial inclusion for millions, backed by solid regulations and cutting-edge blockchain tech. Whether you're eyeing stablecoin savings or global investments without the hassle of traditional banks, Fasset's superapp is reshaping how everyday users and businesses handle digital assets.

Fasset launched in 2019 from Dubai, quickly gaining traction by prioritizing accessibility in underserved markets. What sets it apart in this Fasset review is its dual regulation: VARA oversight in Dubai and now a provisional banking license from Malaysia's Labuan Financial Services Authority. This October 2025 milestone lets Fasset operate a full-service Islamic digital bank within a regulated fintech sandbox. Picture zero-interest savings accounts funded by stablecoins, financing options that align with Islamic finance, and investments in U. S. stocks, gold, or cryptocurrencies, all without riba (interest). It's practical innovation meeting cultural needs head-on.

Fasset's Malaysia License Unlocks Shariah-Compliant Innovation

The Labuan approval is a game-changer for licensed digital asset platforms like Fasset. It greenlights stablecoin-backed services that were once niche dreams. Users now enjoy savings accounts yielding returns through ethical investments, not interest. Add a Visa-linked crypto card compatible with Apple Pay and Google Pay, and you've got everyday usability that rivals big banks. I appreciate how Fasset targets the unbanked in 125 countries, processing over $7 billion in annualized volume as of late 2025, with forecasts doubling by year's end. This isn't hype; it's measurable growth driven by real demand for crypto bank financial inclusion.

From my decade in fintech, platforms succeeding in 2026 share one trait: regulatory trust paired with user-centric design. Fasset nails this. Their superapp simplifies onboarding, letting you swap fiat for stablecoins instantly and invest in tokenized RWAs like real estate or commodities. No more clunky exchanges or high fees; transfers are borderless and near-instant, thanks to smart infrastructure.

Tokenized RWAs: Fasset's Edge in Real-World Asset Access

Diving deeper into Fasset tokenized RWAs, the platform tokenizes assets like gold and equities on blockchain, making them divisible and tradable globally. This democratizes wealth-building. Imagine owning a fraction of U. S. stocks without a brokerage account or custody worries. Fasset's approach leverages stablecoins for stability, crucial amid 2026's regulatory shifts noted in PwC's Global Crypto Report. With FATF standards pushing for better virtual asset oversight, Fasset's compliance positions it ahead of unregulated peers.

The Own network, Fasset's Ethereum Layer 2 on Arbitrum, powers this magic. It handles instant settlements, slashing costs and times for cross-border moves. Businesses love it for treasury management; individuals, for remittances without predatory fees. Serving over 2 million users, Fasset proves scale matters. Projections from The Digital Banker peg annualized volume at $24 billion by 2026 end, fueled by RWA tokenization and stablecoin adoption trends Silicon Valley Bank highlighted.

Borderless Transfers Redefined for Global Users

When it comes to Fasset global transfers, think efficiency at its finest. The platform's infrastructure eliminates intermediaries, enabling peer-to-peer sends in stablecoins that settle in seconds. Pair this with the crypto card, and spending tokenized assets feels native. In regions where banking access lags, Fasset acts as the people's bank in crypto, aligning with 2026 predictions of stablecoin dominance from Chris Skinner's insights. It's not just transfers; it's empowerment, letting users in Asia, Africa, or the Middle East invest confidently.

Critics might question scalability, but Fasset's $7 billion volume and sandbox testing address that. Their Shariah focus taps a $3 trillion Islamic finance market, blending it with blockchain for hybrid appeal. As a CAMS-certified consultant, I see Fasset bridging divides that others ignore, making it a top pick for ethical, efficient digital banking.

Security remains paramount in any Fasset review, and this platform delivers with institutional-grade measures. Built on the Own network's Layer 2 security, Fasset employs multi-signature wallets, cold storage for the majority of assets, and real-time monitoring powered by AI-driven anomaly detection. Their VARA regulation in Dubai demands rigorous KYC and AML protocols, which they've extended to the Malaysia sandbox. No major breaches reported since inception speaks volumes in an industry rife with hacks. For users wary of custody risks, Fasset offers non-custodial options for tokenized RWAs, letting you retain private keys while enjoying platform liquidity.

Fees and Accessibility: Transparent Costs for Everyday Use

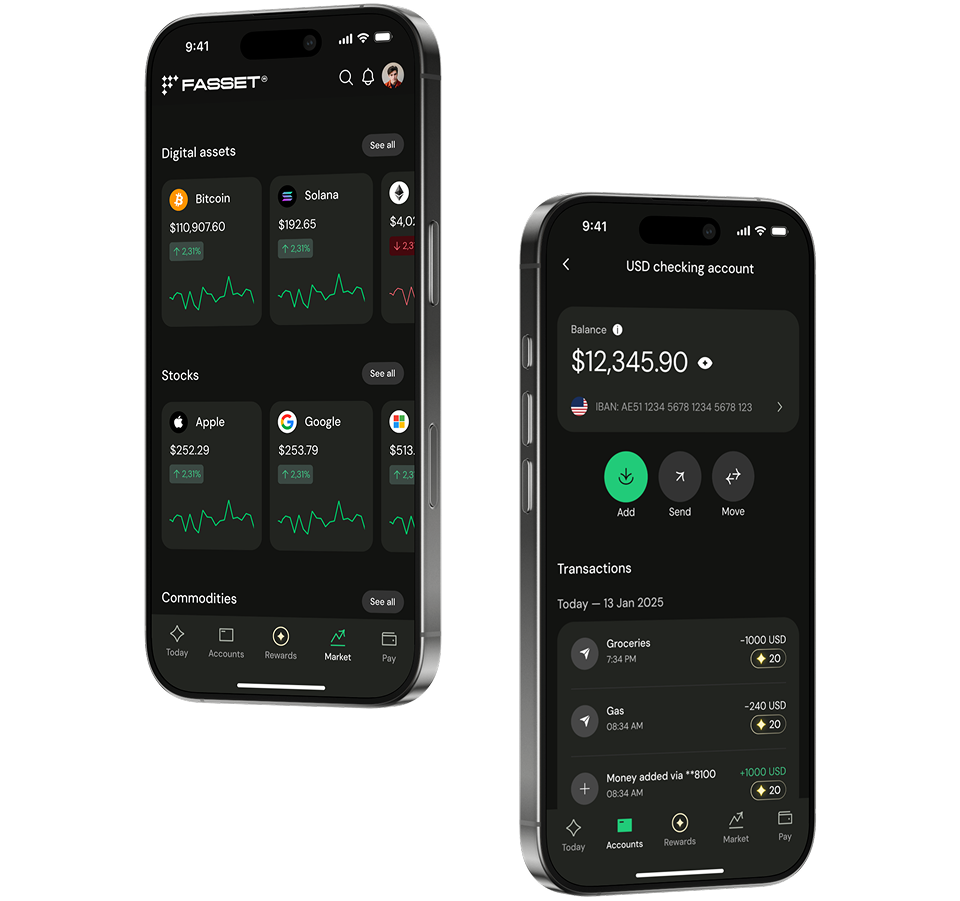

One standout in the Fasset crypto bank ecosystem is its fee structure, designed for affordability. Fiat-to-stablecoin on-ramps carry low spreads around 0.5-1%, competitive against traditional remittance giants. Borderless transfers? Often free or under $1 via stablecoins, a fraction of bank wires. Trading tokenized RWAs incurs maker-taker fees from 0.1%, with zero for stablecoin savings yields derived from ethical halal investments. The Visa crypto card adds 1-2% on spends, but cashback in stablecoins offsets that for frequent users. No hidden charges, no inactivity fees; it's built for the long haul, especially in emerging markets where every cent counts toward crypto bank financial inclusion.

Fasset's Core Features

- Shariah-Compliant Savings: Zero-interest accounts and financing services adhering to Islamic principles, powered by stablecoins.

- Tokenized Gold & U.S. Stocks: Invest in physical gold and U.S. equities through secure, tokenized assets on the Own network.

- Instant Global Transfers: Borderless payments with Ethereum Layer 2 settlements via Arbitrum-based Own network.

- Visa Crypto Card: Spend crypto anywhere with Apple Pay and Google Pay integration.

- RWA Fractional Ownership: Tokenized real-world assets enabling accessible investment in global opportunities.

That transparency builds trust, crucial as global regs tighten per the FSB's thematic review. Fasset's superapp ties it all together: a single dashboard for savings, investments, and payments. Onboard in minutes with biometric verification, then swap currencies or stake RWAs effortlessly. Businesses get API access for treasury automation, projecting that jump to $24 billion volume by 2026.

Pros, Cons, and Who Should Choose Fasset?

Fasset shines for diaspora workers sending home remittances, Muslim investors seeking halal options, and SMEs needing efficient cross-border treasury. If you're in one of 125 supported countries, chasing yields without interest, or tokenizing assets for liquidity, it's ideal. Less so for high-frequency traders wanting deep order books; that's for pure exchanges. Scalability concerns? Their Arbitrum base and sandbox stress tests counter that, aligning with SVB's 2026 RWA tokenization boom.

From agentic AI integrations teased in their roadmap to stablecoin expansions, Fasset eyes the $3 trillion Islamic finance pie while serving all. PwC notes uneven FATF adoption, but Fasset's proactive compliance future-proofs it. In a year of institutional inflows and M and A waves, this licensed digital asset platform avoids the pitfalls plaguing shadow banks.

Users rave about the app's intuitiveness, with 2 million strong proving adoption. Pair ethical finance with blockchain speed, and you get more than a bank; it's a gateway to global opportunity. For anyone prioritizing security, inclusion, and innovation, Fasset redefines what's possible in 2026 digital banking. Dive in, and experience borderless wealth on your terms.

No comments yet. Be the first to share your thoughts!