In the dynamic landscape of 2026, on-chain crypto neobanks have redefined financial services by managing billions in assets through decentralized protocols, eliminating the need for physical branches. Platforms like Aave, Morpho, and Compound Finance exemplify this shift, offering lending, borrowing, and yield generation across multiple chains with institutional-grade security and efficiency. As tokenisation surges toward a trillion-dollar market fueled by money market funds and gold-backed assets, these neobanks aggregate liquidity, automate bridging via ERC-4337 account abstraction, and deliver seamless user experiences that rival traditional banks.

Venture capital flows underscore this momentum; investors target protocols that address real-world risks with niche on-chain assets. Layer-2 dominance, now over 90% of Ethereum activity, amplifies scalability, positioning crypto neobanks 2026 as pivotal in the digital finance revolution. From my vantage as a portfolio strategist, this evolution demands a cautious lens on regulatory horizons, yet the TVL milestones signal robust adoption.

Architectural Pillars Supporting Branchless Billions

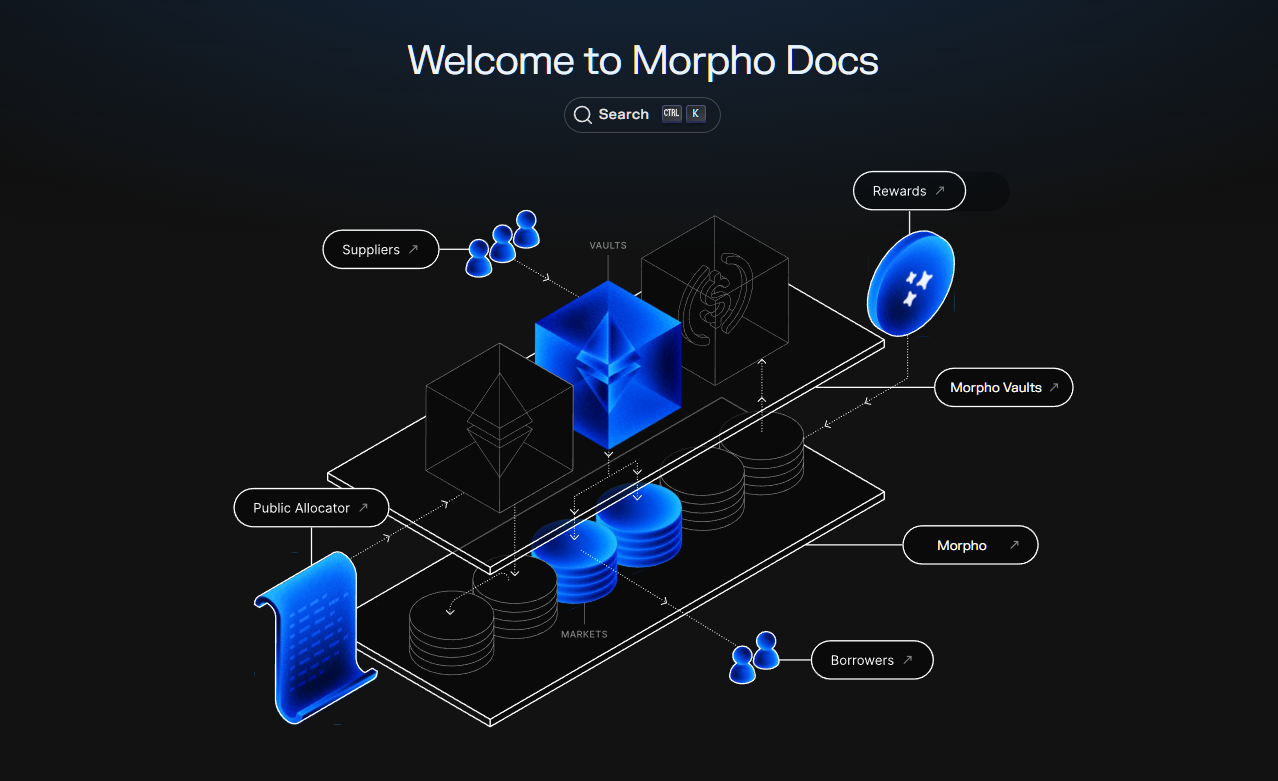

These decentralized crypto banks thrive on core innovations: permissionless access, smart contract automation, and cross-chain interoperability. Aave pioneered flash loans and dynamic interest rates, now managing over $10 billion in TVL through risk-isolated markets. Morpho enhances this with peer-to-peer matching, slashing costs by up to 20% while optimizing capital efficiency. Spark Protocol, integrated deeply with MakerDAO, facilitates DAI-based lending at scale, appealing to institutions seeking collateralized stability.

Institutional adoption defines 2026; on-chain neobanks bridge TradFi gaps without custodial risks.

Compound Finance's composability allows seamless integration into broader DeFi ecosystems, while Kamino Finance on Solana delivers high-throughput liquidity provision. Radiant Capital's omnichain approach unifies lending pools across EVM and non-EVM chains, mitigating fragmentation. This infrastructure not only handles billions but anticipates regulatory scrutiny by embedding compliance layers like optional KYC for high-value transactions.

Comparative TVL and Yield Benchmarks

Assessing these leaders reveals strategic differentiators in TVL growth, supported chains, and yield profiles. Aave's multi-chain dominance contrasts with Liquity's single-protocol focus on overcollateralized loans via LUSD. Gearbox Protocol introduces leveraged vaults, amplifying returns for sophisticated users, while Venus Protocol on BNB Chain leverages low fees for retail influx.

Key DeFi Protocols for On-Chain Crypto Neobanks: TVL, Primary Chains, and Avg Yields (2026)

| Protocol | TVL | Primary Chains | Avg Yield (APY) |

|---|---|---|---|

| Aave | $45.2B | Ethereum, Polygon, Arbitrum, Optimism, Avalanche | 6.8% |

| Morpho | $18.7B | Ethereum, Base | 8.4% |

| Spark Protocol | $9.4B | Ethereum | 7.2% |

| Compound Finance | $7.1B | Ethereum, Base, Polygon | 6.1% |

| Kamino Finance | $4.2B | Solana | 9.5% |

Euler Finance's modular risk framework recovered strongly post-exploits, underscoring resilience. My analysis favors protocols with proven audit histories and governance decentralization, as macroeconomic pressures like interest rate normalization could test borrow demands.

Strategic Imperatives for Institutional Integration

As crypto banks without branches scale, integration with real-world assets becomes paramount. Spark Protocol's ties to tokenized treasuries position it for trillion-dollar tokenisation inflows. Kamino Finance's automated market making rivals centralized exchanges in efficiency, drawing Solana's high-velocity users. Radiant Capital's cross-chain borrowing democratizes access, yet demands vigilant oracle monitoring to avert liquidation cascades.

Venus Protocol benefits from BNB's outperformance, channeling ecosystem liquidity into yields exceeding 15% APY on stables. Euler Finance innovates with sub-accounts for isolated strategies, ideal for portfolio segmentation. Looking ahead, these platforms must navigate MiCA and potential U. S. clarity post-elections, balancing innovation with compliance to sustain billions under management.

Liquity stands apart with its crypto banks without branches ethos, delivering trustless loans backed by ETH collateral at zero protocol fees, amassing billions through LUSD stability. Gearbox Protocol elevates this paradigm via credit accounts that enable leveraged DeFi positions without liquidation risks in volatile markets, attracting yield farmers and institutions alike. Together, these protocols form a resilient ecosystem, where TVL surges reflect not just hype, but genuine utility in on-chain banking assets.

Risk Frameworks and Resilience Metrics

Resilience defines longevity in decentralized finance. Aave's risk isolation via portals prevents cascade failures, a lesson reinforced post-2022 exploits. Morpho's optimizer layer dynamically allocates to highest-efficiency pools, minimizing impermanent loss. Spark Protocol's governance ties to MakerDAO ensure overcollateralization ratios exceed 150%, buffering against oracle deviations. Compound Finance deploys algorithmic oracles for real-time pricing, while Kamino Finance leverages Solana's parallelism for sub-second executions.

Risk Metrics for Key On-Chain Lending Protocols (Radiant Capital, Venus Protocol, Euler Finance, Liquity, Gearbox Protocol)

| Protocol | Liquidation Threshold (%) | Average Collateral Factor (%) | Audit Count |

|---|---|---|---|

| Radiant Capital | 82.5 | 75 | 6 |

| Venus Protocol | 80 | 70 | 8 |

| Euler Finance | 85 | 78 | 10 |

| Liquity | 110 | N/A | 7 |

| Gearbox Protocol | 92.5 | 85 | 5 |

Radiant Capital's chain-agnostic vaults distribute risks across ecosystems, Venus Protocol employs dynamic borrow limits on BNB Chain, and Euler Finance's tiered accounts segregate high-volatility assets. Liquity's minimum 110% collateral ratio enforces conservatism, and Gearbox's composable leverage caps exposure. From a macroeconomic standpoint, these mechanisms position decentralized crypto banks to weather rate hikes or crypto winters, with diversified revenue from origination fees sustaining development.

On-chain neobanks prioritize antifragility; exploits sharpen, not shatter, their foundations.

Yield Strategies and User Onboarding

For retail and institutional users, yield optimization drives adoption. Platforms embed account abstraction for gasless interactions, mirroring neobank UX. Aave's aTokens accrue interest in-wallet, Morpho's vaults auto-compound, and Spark's sDAI offers stable returns pegged to treasuries. Kamino's liquidity lockers incentivize long-term provision, Radiant bridges yield across Cosmos and EVM, while Venus taps BNB liquidity for competitive APYs.

Euler's reactive vaults adjust to market regimes, Liquity provides pure-play ETH yields via stability pools, and Gearbox amplifies via perpetuals integration. Onboarding remains frictionless: wallet connect, collateral deposit, instant liquidity. Yet, strategic users layer these with RWAs, as tokenisation floods protocols with tokenized treasuries and gold, per Aspen Digital's trillion-dollar forecast.

Regulatory tailwinds favor compliant innovators. MiCA's stablecoin rules bolster EU operations, while U. S. frameworks post-2024 elections could unlock trillions in pension allocations. VC inflows, as noted by Binance analyses, target protocols automating bridging and abstraction, fortifying multi-chain dominance.

Investors should prioritize governance participation; Aave's decentralized senate, Compound's timelocks exemplify accountability. My portfolio lens favors diversified exposure via indices or vaults, hedging chain-specific risks. Layer-2 efficiencies, now 90% of Ethereum volume, propel scalability, ensuring these neobanks manage not just billions, but the mainstream transition to programmable money. As crypto neobanks 2026 mature, they redefine sovereignty: your keys, your yields, borderless and branchless.

No comments yet. Be the first to share your thoughts!