The digital banking revolution has entered a new phase: neobanks are rapidly integrating stablecoins to deliver truly instant, borderless payments. What was once the domain of crypto-native users and tech-savvy remitters is now accessible to anyone with a smartphone. This shift is not just about faster transfers; it’s about unlocking global financial inclusion, reducing costs, and providing seamless access to digital dollars for millions in emerging markets.

Why Neobank Stablecoin Integration Is Taking Off

Traditional cross-border payments are notorious for their delays, high fees, and reliance on outdated correspondent banking networks. Stablecoins like USDC and EURC, built on secure blockchain rails, have changed the equation. By pegging their value 1: 1 to fiat currencies, stablecoins offer stability without sacrificing the speed and efficiency of crypto rails.

Neobanks are leveraging these advantages in several ways:

- Global access to stable value: Anyone can hold USD or EUR equivalents without a traditional bank account.

- Instant settlement: Transactions settle in seconds, not days.

- No borders or banking hours: Send or receive payments anytime, anywhere.

- Dramatically lower fees: Especially crucial for remittances and small businesses operating internationally.

- Simplified compliance: On-chain transparency helps automate AML/KYC checks.

The result? Neobanks can now serve as lifelines for users in countries facing currency volatility or limited access to the global financial system. According to recent case studies from TransFi and BVNK, fintech platforms are embedding APIs that let users convert local currency into stablecoins and make instant on-chain transfers worldwide, often bypassing expensive middlemen entirely.

The API-Driven Future: How It Works Under the Hood

The magic lies in smart integrations. Today’s leading neobanks partner with infrastructure providers like Circle (for USDC), BVNK (for embedded wallets), and payment networks such as Visa. These partnerships enable features like:

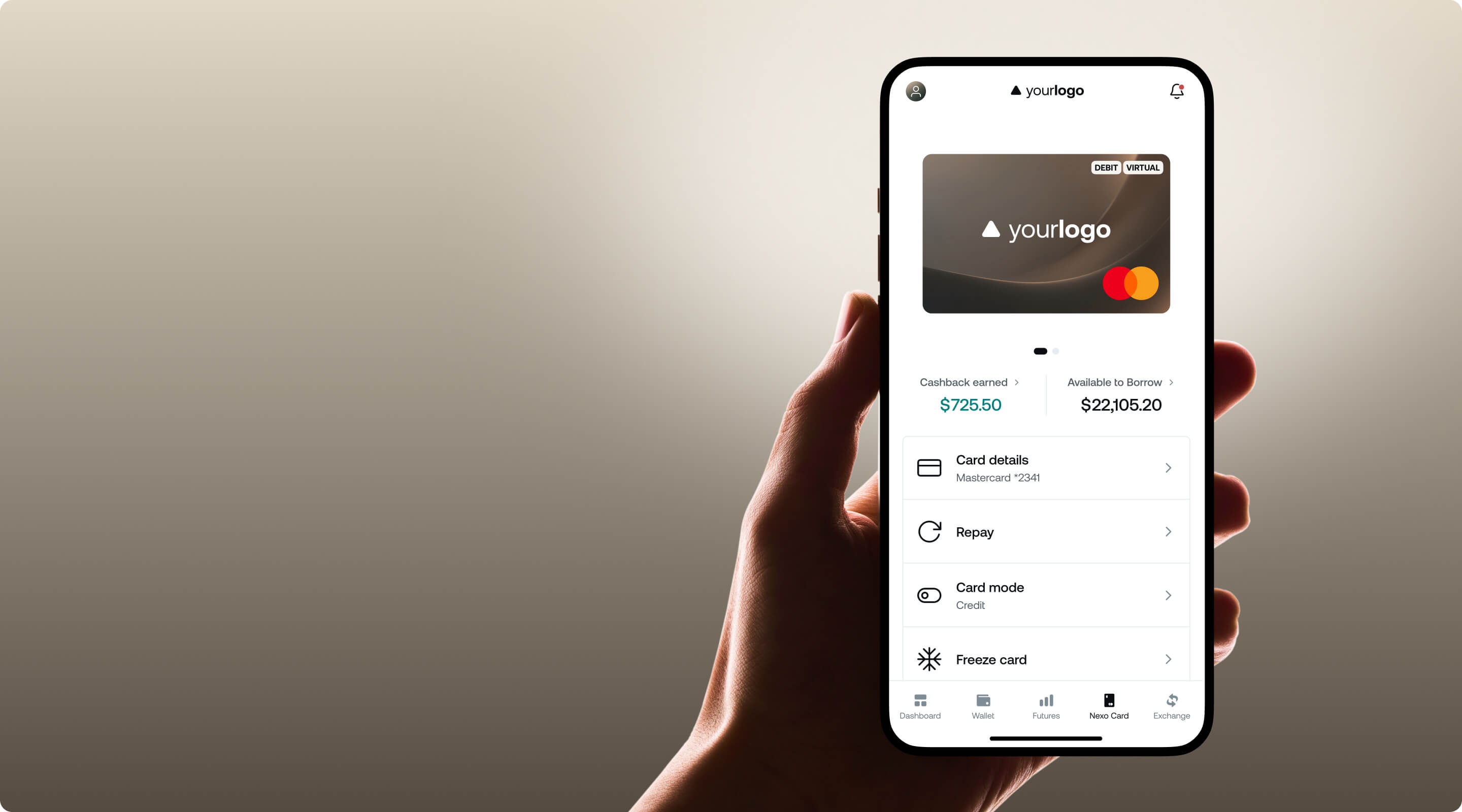

- 1: 1 conversion between fiat and stablecoins: For example, Revolut now lets its 65 million users swap USD directly for USDC at fixed rates up to $578,630 per transaction.

- Embedded multi-currency wallets: Platforms like BVNK unify fiat and stablecoin holdings so customers can send funds over Swift, ACH, or blockchain with a single tap.

- No-code/low-code APIs: Fintechs simply plug into these rails to offer near-instant payouts globally, no need for custom blockchain development.

This architecture dramatically simplifies global money movement. A business in Nigeria can pay a freelancer in Brazil within seconds using USDC, no waiting for wire transfers or worrying about FX swings. For neobanks targeting emerging markets where dollar access is limited or unstable local currencies present risk, this is game-changing.

Banks and Payment Networks Join the Party

The momentum isn’t limited to startups. Established players are jumping on board too. In Europe, ClearBank has joined Circle’s payment network to enable faster settlements using both USDC and EURC. Meanwhile, Visa’s expansion of stablecoin settlement capabilities (notably on Solana and Ethereum) allows merchant acquirers to process real-time cross-border transactions without relying solely on legacy correspondent banks.

This trend is accelerating thanks to regulatory clarity around stablecoins in many jurisdictions, and growing demand from merchants who want cheaper liquidity options. With every new partnership announced, crypto banking cross-border payments get faster, more transparent, and more affordable for end-users worldwide.

What’s especially striking is how neobanks are using these stablecoin rails to offer features that traditional banks simply can’t match. Imagine a gig worker in Argentina receiving USD payments instantly into a digital wallet, or a small business in Kenya settling invoices with partners in Europe without ever touching SWIFT. This isn’t just about speed; it’s about empowering users with direct, programmable access to global finance.

Top 5 Ways Stablecoins Are Transforming Neobanks

- 1. Instant Global Remittances: Neobanks like TransFi enable users to send stablecoin-powered remittances worldwide in seconds, bypassing traditional banking delays and high fees.

- 2. Seamless Cross-Border Payroll: Platforms such as BVNK let businesses pay employees and contractors instantly in USDC or USDT, ensuring fast, reliable global payroll without currency conversion hassles.

- 3. Real-Time FX Savings: Neobanks like Revolut offer 1:1 USD-to-stablecoin swaps, letting users hold and spend digital dollars to avoid local currency volatility and save on foreign exchange fees.

- 4. 24/7 Access to Digital Dollars: With stablecoin integration, customers of neobanks such as neobanque.ch can access, hold, and spend USD, EUR, or GBP anytime, anywhere, even outside traditional banking hours.

- 5. Streamlined Business Payments: Major payment networks like Visa now support stablecoin settlements on blockchains like Solana and Ethereum, enabling neobanks to offer merchants real-time, borderless payments and improved liquidity.

For fintechs and neobanks, these innovations open up new revenue streams and reduce operational friction. By leveraging embedded wallets that combine fiat and stablecoins, platforms can offer customers a choice: settle in local currency or digital dollars, depending on market conditions or personal preference. The result? More resilient banking for individuals and businesses facing currency risk or capital controls.

Real-World Impact: From Emerging Markets to Global Commerce

The impact goes far beyond crypto enthusiasts. In regions where hyperinflation erodes savings or banking infrastructure is patchy at best, stablecoin-powered neobanks are bridging the gap between local economies and the global financial system. According to recent case studies by TransFi, API-driven integrations have enabled millions to convert local currency into USDC instantly, creating safe savings options for families and unlocking new opportunities for entrepreneurs.

This model is also reshaping B2B payments. With instant settlement across borders, businesses can manage cash flow more efficiently and avoid the headaches of international wires or delayed receivables. As more payment networks like Visa and ClearBank adopt stablecoin rails, expect further cost reductions and increased adoption among mainstream merchants.

What’s Next? The Road Ahead for Stablecoin Neobank Partnerships

Looking forward, the lines between crypto-native services and traditional banking will only blur further. As regulatory clarity improves and APIs become even more user-friendly, expect broader adoption of stablecoin neobank partnerships. We’re already seeing innovative use cases emerge:

- Salaries paid in USDC: delivered instantly across continents

- Automated FX hedging within multi-currency wallets

- Real-time merchant settlements using blockchain rails for improved liquidity management

- Lending products collateralized by stablecoins, expanding credit access globally

The competitive landscape is heating up as fintechs race to integrate next-gen payment infrastructure that’s fast, transparent, and borderless by design. For users, from freelancers to global enterprises, the promise of instant global crypto transfers through trusted neobanks is quickly becoming reality.

If you want a deeper dive into how stablecoin-powered banks are bridging DeFi with mainstream finance (and what it means for your business), check out our feature here: How Stablecoin Neobanks Are Bridging DeFi And Traditional Banking: Features and Providers To Watch In 2024.

No comments yet. Be the first to share your thoughts!