Banking is entering a new era in 2025, as tokenized deposits rapidly move from pilot projects to the core of global bank payments infrastructure. These blockchain-based representations of traditional deposits are not just a technical upgrade - they are fundamentally reshaping how money moves between individuals, institutions, and even across borders. Unlike stablecoins, which are typically issued by non-banks and pegged to fiat currencies, tokenized deposits remain legally equivalent to standard bank liabilities while gaining the speed and programmability of digital assets.

The Surge of Tokenized Deposits: Global Adoption Accelerates

In the past twelve months, major banks have announced sweeping initiatives to integrate tokenized deposit solutions. In the UK, banking giants such as HSBC, NatWest, Lloyds, Barclays, Nationwide, and Santander are all targeting a 2026 rollout for tokenized deposit services. This aligns with the Bank of England's strong preference for tokenized deposits over stablecoins, citing their ability to maintain systemic stability within a regulated framework.

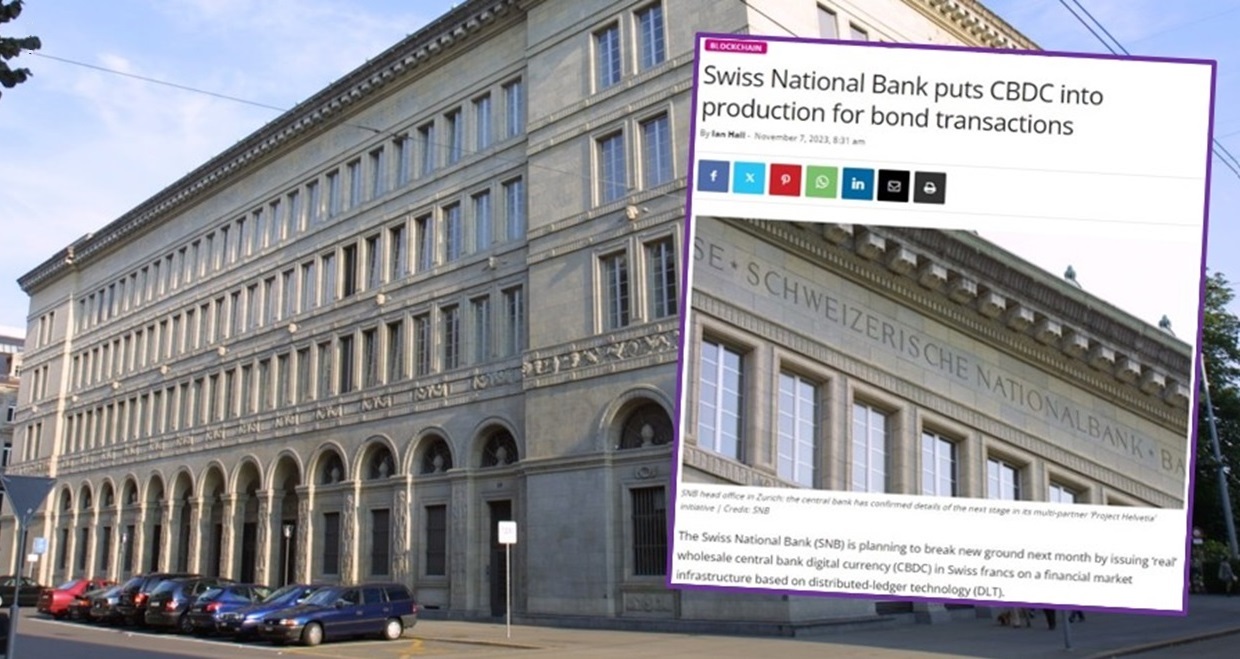

Meanwhile in Switzerland, PostFinance, Sygnum Bank, and UBS have already executed binding payments using bank deposits on public blockchains - a milestone that demonstrates both technical feasibility and regulatory alignment. These successful transactions point toward a near future where interbank settlements can occur instantly around the clock without reliance on legacy clearing systems. For more details on this Swiss breakthrough see Reuters' coverage.

How Tokenized Deposits Work: The Architecture Behind the Shift

The promise of tokenized banking solutions lies in their architecture. When customers deposit funds at a participating bank, those balances can be represented as tokens on permissioned or public blockchains. These tokens are fully backed by central bank reserves or commercial bank balances - ensuring that each digital unit is redeemable 1: 1 for fiat currency. Crucially, unlike stablecoins issued by crypto-native firms (which may face redemption risk or regulatory scrutiny), tokenized deposits inherit the creditworthiness and legal protections of their parent banks.

This structure enables several advantages:

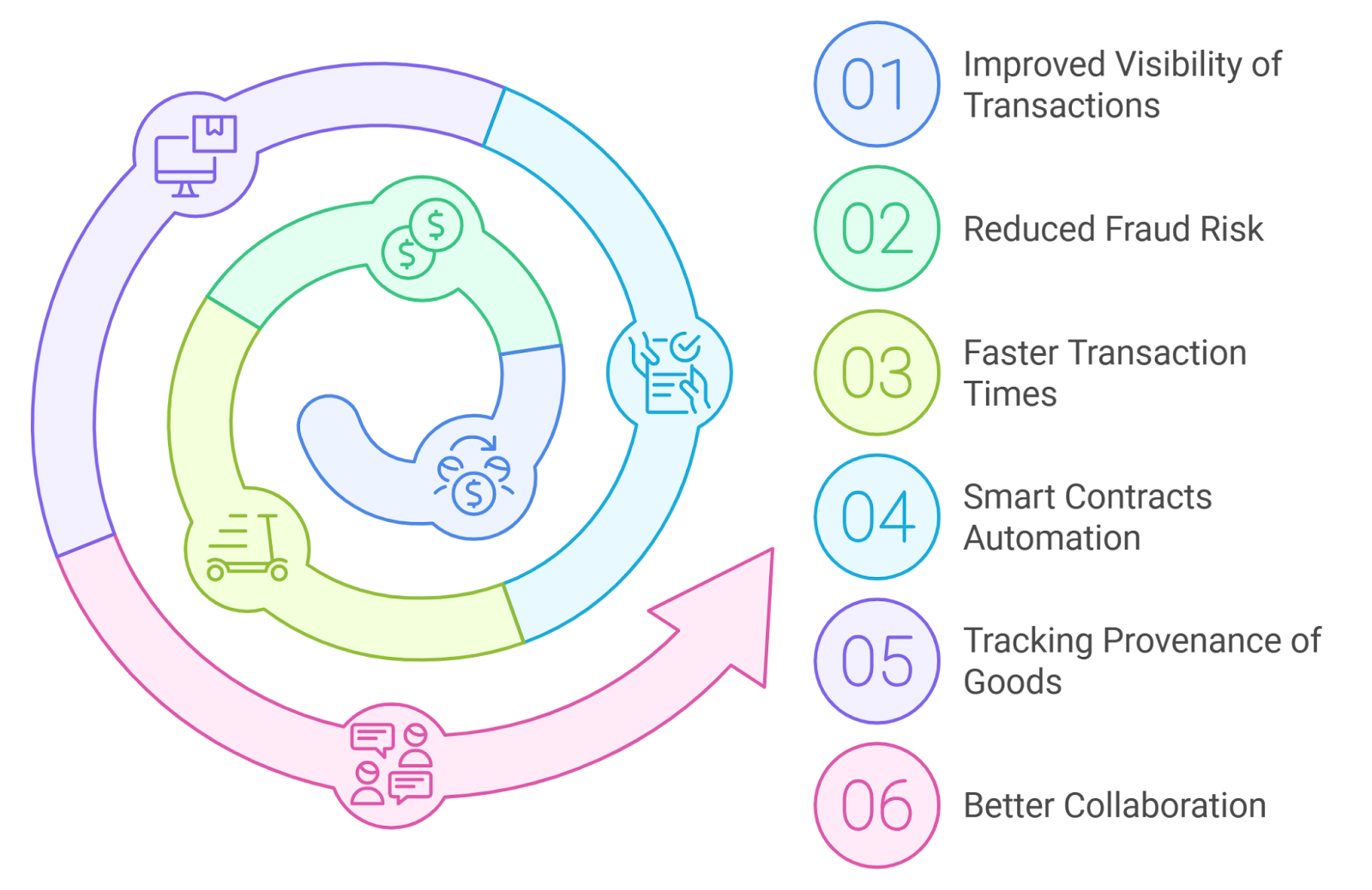

Key Benefits of Tokenized Deposits for Banks and Customers

- Instant Settlement and 24/7 Payments: Tokenized deposits enable real-time, around-the-clock payments, eliminating delays associated with traditional systems like ACH or Fedwire. This allows banks and customers to transfer funds instantly, even outside regular banking hours.

- Enhanced Security and Transparency: By leveraging blockchain technology, tokenized deposits provide a secure, tamper-resistant ledger for transactions. This increases transparency for both banks and customers, reducing the risk of fraud and errors.

- Lower Transaction Costs: Tokenized deposits streamline payment processes by reducing intermediaries, leading to lower operational and transaction costs for banks. Customers benefit from reduced fees and faster service.

- Programmable and Flexible Payments: Tokenized deposits enable programmable money, allowing banks and customers to automate complex payment workflows, such as conditional payments or recurring transfers, enhancing efficiency and customization.

- Improved Cross-Border Payment Efficiency: Banks using tokenized deposits can facilitate seamless cross-border transactions, minimizing settlement times and currency conversion complexities for customers engaged in international commerce.

- Regulatory Clarity and Financial Stability: Tokenized deposits are issued by regulated banks and represent existing deposit liabilities, aligning with central bank preferences (such as the Bank of England) and supporting financial stability within the traditional banking ecosystem.

Banks can now offer real-time settlement between accounts at different institutions without waiting hours or days for ACH or SWIFT batch processing. Payments become programmable - supporting conditional logic such as escrow releases or automated compliance checks directly on-chain. And because these tokens exist within regulated banking environments, they sidestep many of the legal uncertainties that have hindered broader stablecoin adoption.

Programmable Money Meets Regulatory Clarity

The drive toward programmable money is being matched by increasing regulatory clarity around tokenized deposits regulation. Financial technology providers like Finzly are rolling out API-first payment platforms that support both stablecoins and tokenized deposit rails - reflecting surging demand from banks eager to modernize their treasury operations (see Finzly's announcement). This convergence allows banks to compete with fintechs while offering clients familiar legal protections.

The implications for payment infrastructure are profound. Banks no longer need to rely solely on legacy networks like Fedwire or CHAPS; instead they can leverage blockchain’s inherent transparency and resilience. As more jurisdictions clarify supervisory expectations around digital liabilities versus stablecoins or CBDCs (Central Bank Digital Currencies), expect adoption curves to steepen further through 2025.

One of the most compelling aspects of tokenized deposits is their potential to unlock new efficiencies and reduce costs across the entire banking stack. According to Quant, banks could save billions by eliminating intermediaries and batch settlement lags, while also reducing operational risks linked to reconciliation errors and fraud. This not only benefits large financial institutions but also levels the playing field for smaller banks and fintechs seeking to deliver faster, more transparent payment experiences.

Unlike stablecoins, which often operate outside traditional regulatory perimeters, tokenized deposits are fully integrated within existing legal frameworks. This provides both users and regulators with confidence that digital balances remain subject to established consumer protections and oversight. As highlighted by the Bank of England’s stance, this distinction is crucial in preserving financial stability as digital assets proliferate.

CBDCs vs Tokenized Deposits: Strategic Divergence in 2025

The debate over CBDCs vs tokenized deposits continues to shape policy conversations in 2025. While both aim to digitize money for a modern economy, their underlying models diverge sharply. CBDCs represent direct claims on central banks, raising questions about privacy, competition with commercial lenders, and systemic risk during periods of stress. Tokenized deposits, on the other hand, reinforce the existing two-tier banking system by keeping customer funds within regulated commercial banks while leveraging blockchain’s programmability.

This approach appeals to many policymakers because it minimizes disruption while enabling innovation. In practice, it allows banks to offer programmable payments, such as automated payroll or supply chain settlements, without ceding control of monetary policy or deposit flows to non-bank actors or central authorities.

Challenges Ahead: Interoperability and Regulation

Despite rapid progress, several hurdles remain before tokenized banking solutions reach full maturity. Interoperability between different bank blockchains, or between public and permissioned networks, remains a technical challenge that industry consortia are racing to address. Regulatory harmonization is another critical factor: differing approaches across jurisdictions could fragment liquidity or create compliance bottlenecks if not carefully managed.

There’s also the question of customer trust and education. For mass adoption, banks must clearly communicate how tokenized deposits work, and how they differ from stablecoins or CBDCs, to avoid confusion and build confidence in digital rails. Institutions that invest early in transparent user experiences will be best positioned as adoption accelerates.

What’s Next for Crypto Banks?

The rise of tokenized deposits is catalyzing a broader rethink of what it means to be a bank in the digital age. As crypto banks evolve their platforms around programmable money and real-time settlement capabilities, expect new business models centered on embedded finance, open APIs, and global liquidity networks.

For both retail customers and institutional treasurers, this means access to faster payments, lower fees, enhanced transparency, and ultimately greater control over how money moves across borders or between counterparties. The next wave of innovation will likely see partnerships between traditional banks, fintechs, and even non-financial enterprises as programmable deposit rails become a standard feature rather than a niche offering.

Top Strategic Priorities for Banks Adopting Tokenized Deposits

- 1. Ensuring Regulatory Compliance and Financial StabilityBanks must prioritize alignment with evolving regulations, such as the Bank of England’s preference for tokenized deposits over stablecoins, to safeguard financial stability and maintain trust within the regulated ecosystem.

- 2. Seamless Integration with Existing Payment SystemsIntegrating tokenized deposits with legacy rails like ACH and Fedwire is critical. Institutions such as HSBC and UBS are leading efforts to enable interoperability between blockchain-based tokens and traditional banking infrastructure.

- 3. Building Secure, Scalable Blockchain InfrastructureAdopting robust blockchain solutions is essential for instant, secure settlements. Swiss banks, including Sygnum Bank and UBS, have demonstrated the importance of scalable infrastructure by executing binding payments on public blockchains.

- 4. Developing Programmable Money CapabilitiesBanks should invest in programmable payment features—such as those offered by Finzly’s API-first platform—to meet growing demand for automation, conditional payments, and 24/7 settlement.

- 5. Enhancing Customer Experience and Digital OfferingsTo stay competitive, banks must leverage tokenized deposits to deliver faster, more transparent, and cost-effective payment solutions, positioning themselves against emerging digital payment platforms.

The landscape is shifting quickly, but one thing is clear: tokenized deposits are no longer just an experiment at the fringe of finance. In 2025’s competitive environment for crypto banks, those who embrace this technology will set the pace for efficiency, security, and adaptability in global payments infrastructure.

No comments yet. Be the first to share your thoughts!