Picture a world where moving money between accounts is as simple as sending a text, and programmable logic ensures payments happen instantly, securely, and exactly when you intend. This vision is quickly becoming reality through programmable bank accounts, an innovation rapidly transforming the landscape of direct account-to-account crypto payments. As of September 2025, Bitcoin sits at $115,726.00 and Ethereum at $4,476.34, underscoring the scale and maturity digital assets have achieved. Yet it’s not just price action that’s reshaping finance - it’s the infrastructure quietly evolving beneath the surface.

The Rise of Programmable Bank Accounts: Bridging Old and New

Traditional banks are now converging with blockchain-powered platforms to create a new breed of accounts that can execute rules-based transactions without human intervention. These programmable bank accounts go far beyond basic transfers. They allow users to automate payroll, recurring bills, treasury operations, or even trigger multi-party settlements based on smart contract logic.

Key players are already making waves:

Leaders in Programmable Bank Account Innovation

- Kinexys Digital Payments: Kinexys offers an intuitive, self-serve platform that automates global payments 24/7 in near real time. Their scalable network of blockchain deposit accounts enables direct, programmable account-to-account payments, optimizing liquidity and streamlining workflows. Learn more.

- NOAH: NOAH provides virtual accounts that let businesses accept local currency bank transfers, which are automatically converted to cryptocurrencies. This seamless fiat-to-crypto conversion reduces operational costs and eliminates delays, making crypto onramps more efficient. Learn more.

- Bridge: Bridge delivers programmable virtual accounts that act as permanent, reusable fiat deposit addresses. Incoming fiat is instantly converted to crypto and delivered to specified destinations, supporting multiple currencies and local banking details. Learn more.

- P100: P100 offers crypto-friendly EUR business accounts tailored for companies in the digital asset space. Businesses can manage both fiat and crypto, accept global payments, and operate securely within a single platform. Learn more.

NOAH’s virtual account solution lets businesses accept fiat via local transfer and receive instant crypto conversion - a crucial step for global firms seeking to bypass slow onramps and costly intermediaries. Meanwhile, Bridge's virtual accounts offer permanent deposit addresses that auto-convert incoming fiat into crypto in real time.

Programmable Payments in Action: Real-World Use Cases

The headline feature of these next-gen accounts is automation. Imagine payroll that executes itself every Friday afternoon in USDC or BTC - no manual steps required. Or think about e-commerce refunds processed instantly via stablecoins when a return is approved programmatically by a smart contract.

This isn’t just theoretical. Kinexys Digital Payments by J. P. Morgan provides an intuitive self-serve platform for automating global payments 24/7 in near real time while optimizing liquidity management. Smarty Pay enables seamless balance recharges using stablecoins for always-on business operations (see more here). And P100 offers EUR business accounts tailored for crypto-native companies to manage both fiat and digital assets securely (details here).

Beyond Card Networks: Direct Crypto Payments at the Checkout

The consumer experience is also being reimagined. Instead of tapping a plastic card or waiting for ACH settlement delays, programmable bank accounts enable direct account-to-account crypto payments at point-of-sale - often just by tapping your phone or scanning a QR code. This leap eliminates card network fees and puts control back into users' hands while enabling instant settlement for merchants.

The integration between traditional payment giants like Visa Direct and Coinbase is closing the gap between legacy rails and blockchain-powered finance (read more here). The result? Real-time access to funds for trading or spending directly from your bank or exchange balance - no waiting required.

For businesses, the ability to automate complex payment workflows means treasury teams can optimize liquidity around the clock, reduce manual errors, and achieve compliance with programmable audit trails. Stablecoins like USDC and programmable deposit tokens are at the heart of this shift, letting funds move at software speed while maintaining traditional financial safeguards. As noted by Datos Insights, the true revolution is not just digital currency itself but the automation of treasury operations 24/7.

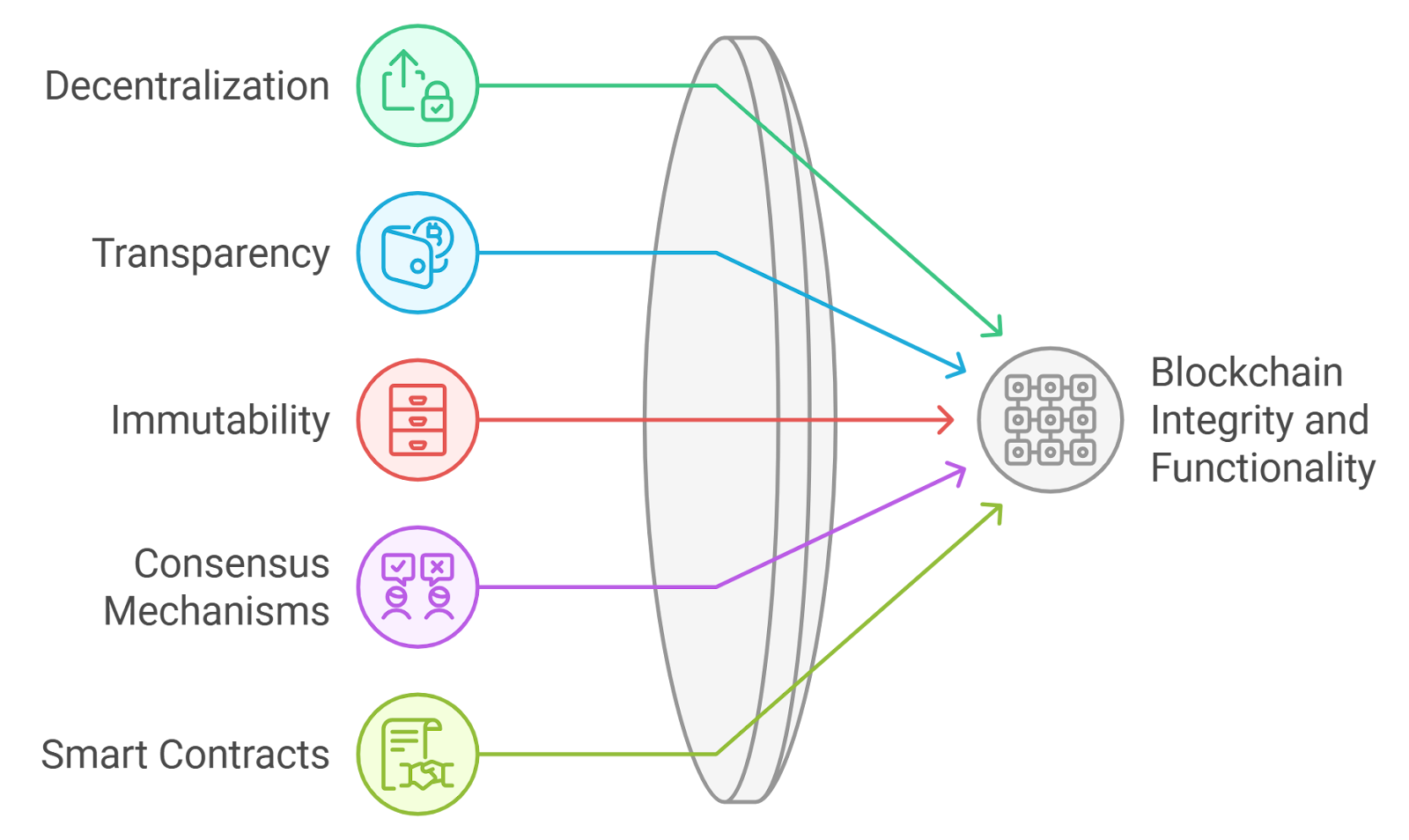

Transparency is another critical benefit. With blockchain-powered programmable accounts, every transaction is traceable and auditable in real time. This aids regulatory compliance and builds trust among users and counterparties. It also paves the way for more sophisticated financial products: think escrow arrangements, milestone-based payouts for freelancers, or dynamic insurance claims that pay out automatically when conditions are met.

Market Signals: Crypto Prices Reflect Growing Maturity

The infrastructure improvements behind programmable bank accounts are arriving at a time when crypto markets themselves have matured significantly. As of September 20,2025:

Bitcoin remains above $115,000, currently trading at $115,726.00 after a modest -0.95% dip in 24 hours. Ethereum holds firm at $4,476.34, down -1.28%. These prices signal not only investor confidence but also growing institutional adoption of programmable money mechanisms.

Key Advantages of Programmable Bank Accounts for Direct Crypto Payments

Top 5 Benefits of Programmable Bank Accounts

- 1. Real-Time, Automated Payments: Platforms like Kinexys Digital Payments enable businesses and consumers to automate global payments 24/7, streamlining workflows and optimizing liquidity with near real-time settlement.

- 2. Seamless Fiat-to-Crypto Conversion: Solutions such as NOAH's Virtual Accounts allow businesses to accept local currency bank transfers that are instantly converted to cryptocurrencies, eliminating conversion delays and reducing operational costs.

- 3. Direct Account-to-Account Transfers Without Cards: With integrations like Visa Direct and Coinbase, users can move funds directly between accounts for immediate access—no physical cards required—enhancing convenience at checkout and for digital payments.

- 4. Enhanced Transparency and Security via Smart Contracts: Leveraging blockchain-based smart contracts, as highlighted by the Federal Reserve Bank of Atlanta, programmable accounts provide transparent, auditable transactions and reduce the risk of fraud or errors in payment processing.

- 5. Flexible Crypto-Friendly Business Banking: Providers like P100 offer business accounts designed for seamless management of both fiat and digital assets, enabling global operations and acceptance of crypto payments within a secure, regulated environment.

This convergence of crypto-native programmability with banking-grade reliability is setting new standards across industries:

- E-commerce: Instant refunds and loyalty payouts via smart contracts.

- Payroll: Automated salary disbursement in fiat or crypto with built-in compliance checks.

- Cross-border trade: Real-time settlement without correspondent banking delays or FX friction.

- Treasury management: Continuous optimization of cash positions using automated triggers.

- B2B payments: Multi-party settlements executed transparently without intermediaries.

Looking Ahead: The Next Chapter in Banking Payments

The adoption curve for programmable bank accounts is accelerating as more banks integrate blockchain rails into their core infrastructure. The line between traditional finance and decentralized protocols will continue to blur as new use cases emerge - from instant cross-border remittance to decentralized payroll systems for global teams.

The next wave will likely see even deeper integration with CBDCs (central bank digital currencies) and interoperable stablecoins that move frictionlessly across networks and jurisdictions. For both individuals and enterprises navigating this landscape, understanding how to leverage these accounts will be key to unlocking faster settlement times, lower costs, and unprecedented control over financial workflows.

The future of direct account-to-account crypto payments isn’t just about speed or cost savings - it’s about programmable trust built into every transaction layer. With innovation from leaders like Kinexys Digital Payments, NOAH, Bridge, P100 and major partnerships such as Visa Direct x Coinbase shaping the field, now is the time to rethink what your business or personal finances could look like when money truly moves at the speed of code.

No comments yet. Be the first to share your thoughts!